Image

Description

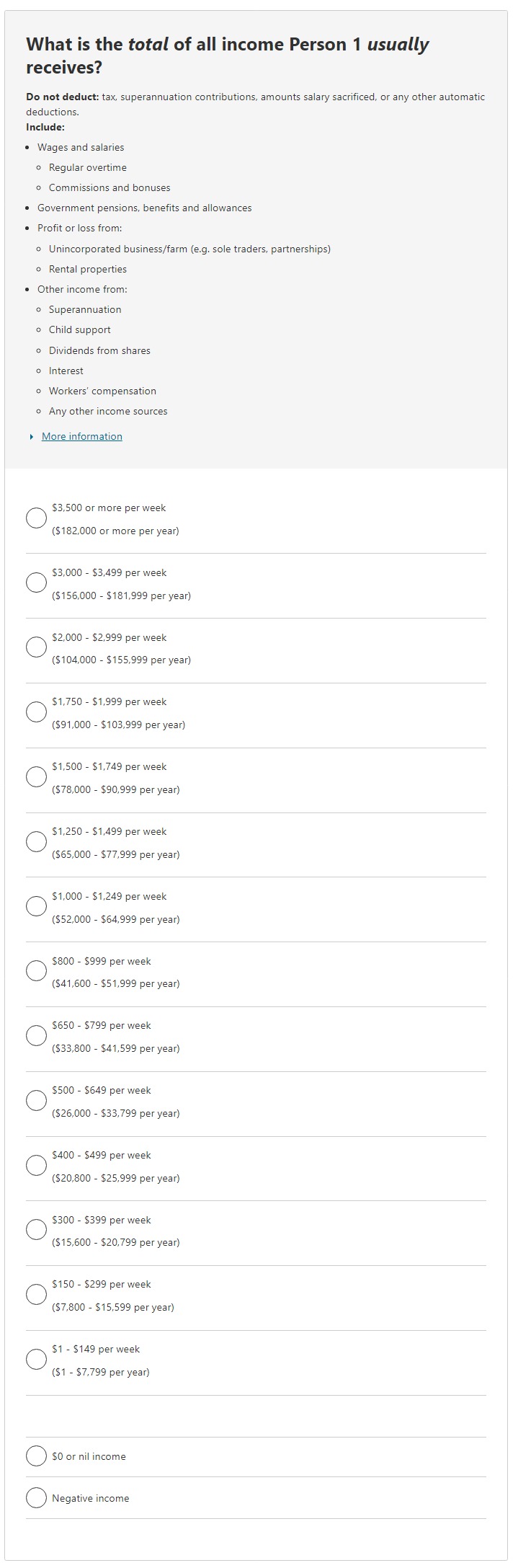

What is the total of all income Person 1 usually receives?

Do not deduct: tax, superannuation contributions, amounts salary sacrificed, or any other automatic deductions.

Include:

• Wages and salaries

• Regular overtime

• Commissions and bonuses

• Government pensions, benefits and allowances

• Profit or loss from:

• Unincorporated business/farm (e.g. sole traders, partnerships)

• Rental properties

• Other income from:

• Superannuation

• Child support

• Dividends from shares

• Interest

• Workers’ compensation

• Any other income sources

• More information

• Person's usual total income

$3,500 or more per week

($182,000 or more per year)

$3,000 - $3,499 per week

($156,000 - $181,999 per year)

$2,000 - $2,999 per week

($104,000 - $155,999 per year)

$1,750 - $1,999 per week

($91,000 - $103,999 per year)

$1,500 - $1,749 per week

($78,000 - $90,999 per year)

$1,250 - $1,499 per week

($65,000 - $77,999 per year)

$1,000 - $1,249 per week

($52,000 - $64,999 per year)

$800 - $999 per week

($41,600 - $51,999 per year)

$650 - $799 per week

($33,800 - $41,599 per year)

$500 - $649 per week

($26,000 - $33,799 per year)

$400 - $499 per week

($20,800 - $25,999 per year)

$300 - $399 per week

($15,600 - $20,799 per year)

$150 - $299 per week

($7,800 - $15,599 per year)

$1 - $149 per week

($1 - $7,799 per year)

$0 or nil income

Negative income

More Information

Image

Description

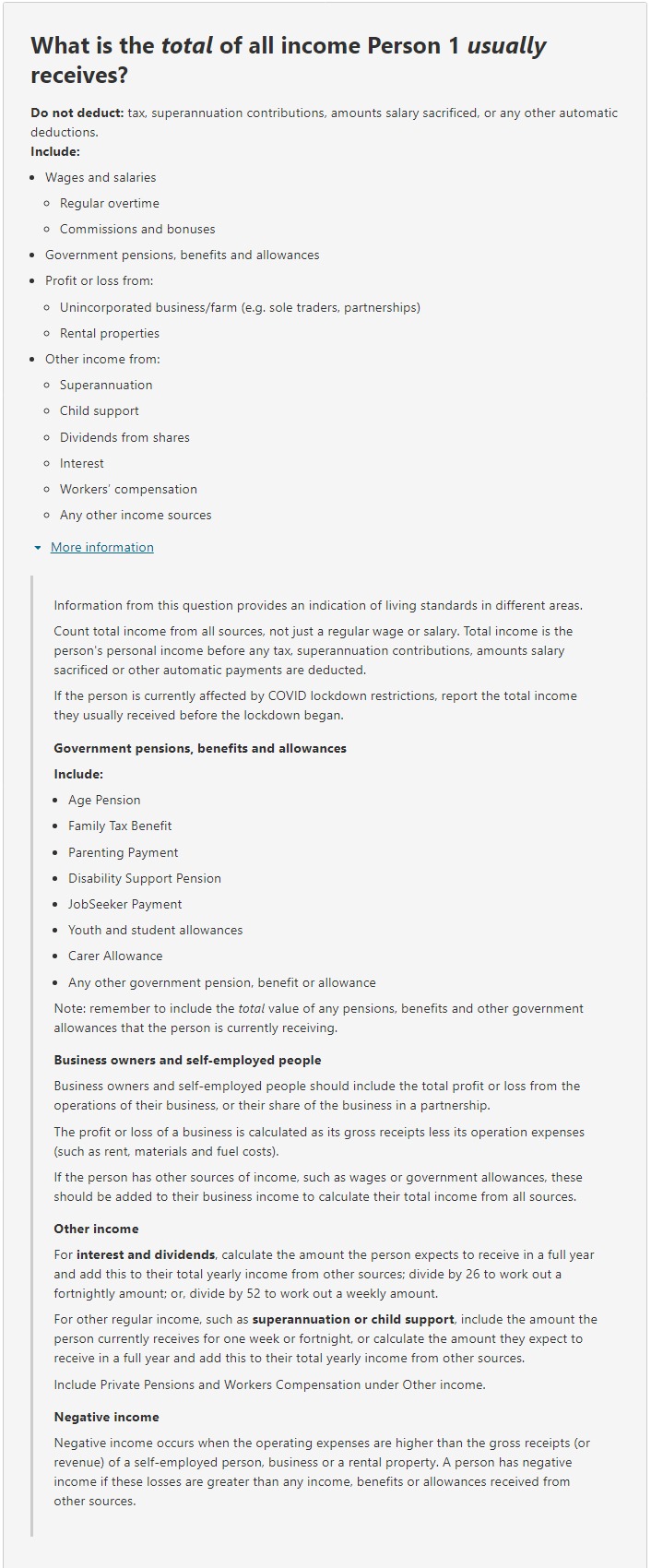

What is the total of all income Person 1 usually receives?

Do not deduct: tax, superannuation contributions, amounts salary sacrificed, or any other automatic deductions.

Include:

• Wages and salaries

• Regular overtime

• Commissions and bonuses

• Government pensions, benefits and allowances

• Profit or loss from:

• Unincorporated business/farm (e.g. sole traders, partnerships)

• Rental properties

• Other income from:

• Superannuation

• Child support

• Dividends from shares

• Interest

• Workers’ compensation

• Any other income sources

More information

Information from this question provides an indication of living standards in different areas.

Count total income from all sources, not just a regular wage or salary. Total income is the person's personal income before any tax, superannuation contributions, amounts salary sacrificed or other automatic payments are deducted.

If the person is currently affected by COVID lockdown restrictions, report the total income they usually received before the lockdown began.

Government pensions, benefits and allowances

Include:

• Age Pension

• Family Tax Benefit

• Parenting Payment

• Disability Support Pension

• JobSeeker Payment

• Youth and student allowances

• Carer Allowance

• Any other government pension, benefit or allowance

Note: remember to include the total value of any pensions, benefits and other government allowances that the person is currently receiving.

Business owners and self-employed people

Business owners and self-employed people should include the total profit or loss from the operations of their business, or their share of the business in a partnership.

The profit or loss of a business is calculated as its gross receipts less its operation expenses (such as rent, materials and fuel costs).

If the person has other sources of income, such as wages or government allowances, these should be added to their business income to calculate their total income from all sources.

Other income

For interest and dividends, calculate the amount the person expects to receive in a full year and add this to their total yearly income from other sources; divide by 26 to work out a fortnightly amount; or, divide by 52 to work out a weekly amount.

For other regular income, such as superannuation or child support, include the amount the person currently receives for one week or fortnight, or calculate the amount they expect to receive in a full year and add this to their total yearly income from other sources.

Include Private Pensions and Workers Compensation under Other income.

Negative income

Negative income occurs when the operating expenses are higher than the gross receipts (or revenue) of a self-employed person, business or a rental property. A person has negative income if these losses are greater than any income, benefits or allowances received from other sources.