Part C - The treatment of contingent liabilities in GFS

13.75.

Paragraph 7.251 of the IMF GFSM 2014 defines contingent liabilities as obligations that do not arise unless a particular, discrete event(s) occurs in the future. The key difference between contingent liabilities and actual liabilities is one or more conditions must be fulfilled before a financial transaction is recorded. With contingent liabilities, there is uncertainty whether a liability will need to be recognised and the size of the payment involved. With actual liabilities, the debt is owned by the borrower and repayment is contractually certain. To manage liquidity the government needs to keep track of contingent liabilities to ensure that there are adequate reserves of funds prepared in case a guarantee is called or other event occurs. The value of explicit contingent liabilities is not included on the GFS balance sheet, but is recorded as a memorandum item in GFS. Memorandum items in GFS differ to those of commercial accounting in that they are compulsory rather than optional.

13.76.

Common types of contingent liabilities are guarantees of payment by a third party, such as when a general government unit guarantees the repayment of a loan by another borrower. In this case, the liability is contingent because the guarantor (the general government unit) is only required to repay the loan if the borrower defaults. Therefore for GFS purposes, the contingent liability will not appear in the accounts of the general government unit unless, and until the guarantee is called.

Explicit contingent liabilities and implicit contingent liabilities

13.77.

In GFS, a distinction is made between explicit contingent liabilities and implicit contingent liabilities. Paragraph 7.252 of the IMF GFSM 2014 defines these as:

- Explicit contingent liabilities are defined as legal or contractual financial arrangements that give rise to conditional requirements to make payments of economic value. The requirements become effective if one or more stipulated conditions arise. Explicit contingent liabilities may take a variety of forms, but guarantees are the most common type.

- Implicit contingent liabilities are defined as not arising from a legal or contractual source but are recognised after a condition or event is realised. The most common form of implicit contingent liability for government is the assumption of provisions for future benefits such as age or disability pensions for a population. Another example is the expectation for the provision of funds for disaster recovery for events that have not yet occurred. Implicit contingent liabilities are not recorded in GFS unless the conditions associated with these are met (e.g. a person reaches an age where they are eligible to claim the age pension). Then the implicit contingent liability transforms into an actual liability and enters the GFS balance sheet. The remainder of this section will deal exclusively with explicit contingent liabilities.

13.78.

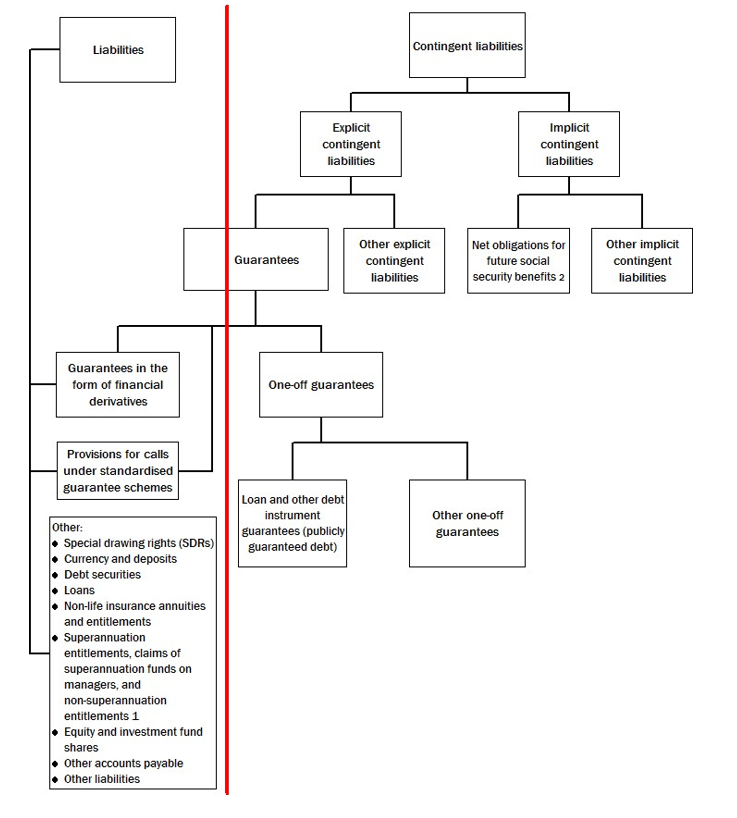

Diagram 13.4 below shows the separation between actual liabilities and contingent liabilities in macroeconomic statistics. The line down the middle delineates the border between the types of liabilities considered actual liabilities and contingent liabilities in GFS.

Diagram 13.4 - Actual and contingent liabilities in macroeconomic statistics

Image

Description

¹Includes liabilities for non-autonomous unfunded employer superannuation schemes

²Excludes liabilities for non-autonomous unfunded employer superannuation schemes

Source: Adapted from Figure 7.2, International Monetary Fund Government Finance Statistics manual, 2014.

Explicit contingent liabilities

13.79.

Although guarantees are the most common type of explicit contingent liabilities, not all guarantees are contingent liabilities. Paragraph 7.253 of the IMF GFSM 2014 notes that guarantees in the form of derivatives and provisions for calls under standardised guarantee schemes are treated as actual liabilities and are recorded on the GFS balance sheet. Paragraph 7.254 of the IMF GFSM 2014 states that explicit contingent liabilities in GFS comprise:

- Publicly guaranteed debt;

- Other one-off guarantees; and

- Explicit contingent liabilities not elsewhere classified.

Publicly guaranteed debt

13.80.

Publicly guaranteed debt are one-off guarantees in the form of loan and other debt instrument guarantees. Paragraph 7.256 of the IMF GFSM 2014 defines one-off guarantees as individual agreements whose associated monetary risk cannot be determined accurately. Often, one-off guarantees involve very large values, and carry a high risk of the guarantee being called. Paragraph 7.257 of the IMF GFSM 2014 notes that one-off guarantees are considered to be a contingent liability of the guarantor. The liabilities under a one-off guarantee continue to be attributed to the debtor unless and until the guarantee is called.

13.81.

Some very high risk one-off guarantees are treated as if they are called at inception. Paragraph 7.258 of the IMF GFSM 2014 gives the example of a one-off guarantee granted by government to a corporation which is experiencing severe financial distress. In this type of case, the liability of the debtor (the corporation in financial distress) is assumed instantly by the guarantor (the government). Paragraph 7.258 of the IMF GFSM 2014 warns against the double counting of one-off guarantees called at inception because although the liability is created by the debtor, it is not owned by them. In this situation, the liability is instantly recorded by the guarantor at the inception of the one-off guarantee.

13.82.

Paragraph 7.259 of the IMF GFSM 2014 groups one-off guarantees into:

- Loan and other debt instrument guarantees in the form of publicly guaranteed debt - these constitute the debt liabilities of public and private sector units, the servicing of which is contractually guaranteed by public sector units. Under this arrangement, one party agrees to bear the risk of non-payment of a financial commitment by another party under a guarantee arrangement. The guarantor is only required to make a payment if the debtor defaults; and

- Other one-off guarantees - these include credit guarantees such as lines of credit and loan commitments, contingent 'credit availability' guarantees, and contingent credit facilities. Lines of credit and loan commitments are one-off guarantee arrangements generally offered by financial institutions (such as banks) which provide a guarantee that undrawn funds will be available in the future, but no liability or financial asset will exist until such funds are actually provided.

13.83.

Paragraph 7.260 of the IMF GFSM 2014 notes that publicly guaranteed debt differs from other types of one-off guarantee because the guarantor guarantees the servicing of the existing debt of other public and private sector units. With other one off guarantees, no liability / financial asset exists until funds are provided or advanced.

Other one-off guarantees

13.84.

Other one-off guarantees form a part of explicit contingent liabilities and are defined in paragraph 7.254 of the IMF GFSM 2014 as comprising one-off guarantees other than publicly guaranteed debt.

Explicit contingent liabilities not elsewhere classified

13.85.

Explicit contingent liabilities not elsewhere classified also form a part of explicit contingent liabilities and are defined in paragraph 7.254 of the IMF GFSM 2014 as explicit contingent liabilities that are not in the form of guarantees. They comprise:

- Potential legal claims stemming from pending court cases;

- Indemnities, which are commitments to accept the risk of loss or damage another party might suffer (for example, indemnities arising in government contracts with other units);

- Uncalled capital, which is an obligation to provide additional capital on demand, to an entity of which it is a shareholder (such as an international financial institution); and

- Potential payments remitting from PPP arrangements.