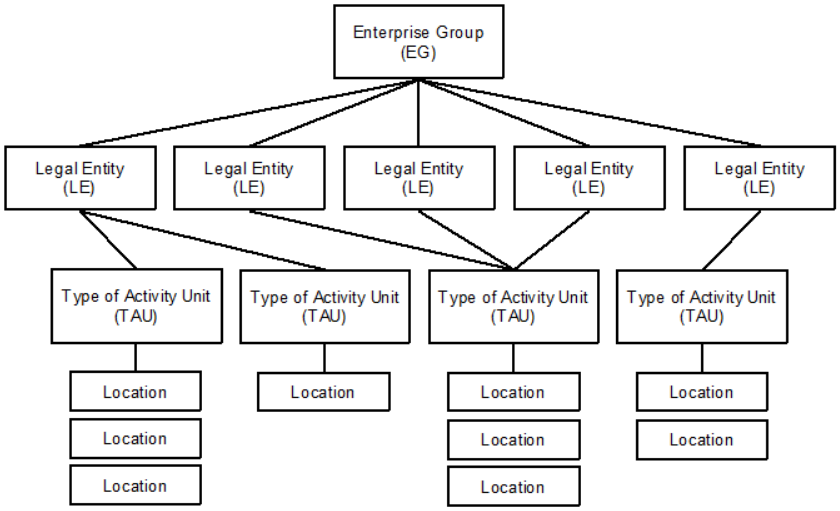

The scope of ABS labour-related surveys varies across collections. Most ABS labour-related business surveys draw upon the ABS Business Register (ABSBR), which is sourced from the Australian Taxation Office's Australian Business Register (ABR). The scope of surveys which use the business register is restricted by the scope and coverage of the register itself (as outlined in the next section). Surveys with broader or different scope are required to either supplement the business register, or use a sample that has been composed independently of the register by using relevant alternative data sources.

The following groups are generally excluded from labour-related business surveys:

- Employing businesses in the Agriculture, Forestry and Fishing industry (Australian and New Zealand Standard Industrial Classification (ANZSIC) Division A), in line with the International Labour Organisation (ILO) Resolution from the Twelfth International Conference of Labour Statisticians 1973. Given that "hired labour constitutes only a minor part of total labour input" in this industry, it would be disproportionately costly to survey a sufficient number of these businesses to obtain a sample of employees to adequately represent this industry.

- Private households employing staff (ANZSIC subdivision 96). Not all private households employing staff are required to register with the Australian Taxation Office (ATO), and as a result of this there is incomplete coverage on the business register and these units are excluded.

- Foreign government representation in Australia (ANZSIC class 7552). Practical collection difficulties and the low numbers of Australian employees involved have resulted in the exclusion of this industry group from the labour-related business surveys.

- Members of Australian permanent defence forces.

- Employing organisations located outside Australia.