- SNA, 2008, para.4.2.

SNA, 2008, para.4.38.

This is not the latest release View the latest release

Chapter 4 Institutional units and sectors

Australian System of National Accounts: Concepts, Sources and Methods

Reference period

2020-21 financial year

Released

9/07/2021

Institutional units

4.1 In any economy, economic activity is undertaken by a variety of transactors. Corporations (both financial and non-financial), government units, households and non-profit institutions all engage in economic activity, but their economic objectives, functions and behaviour differ. For example:

- Corporations are created for the purpose of producing goods or services for the market at economically significant prices, usually as a source of profits for the units that own them. They undertake either production or accumulation (or both), but do not undertake final consumption. They are divided between those mainly providing financial services and those mainly providing goods or non-financial services.

- Non-profit institutions (NPIs) are created for the purpose of producing or distributing goods or services, but not for the purpose of generating income or profits for the units that control or finance them. They are diverse in nature with some behaving like corporations, some are effectively part of general government and some undertake activities similar to general government but are independent of it.

- Government units organise and finance the provision of non-market goods and services to individual households and the community at large, mainly financed out of taxation revenue. They are also concerned with the distribution and redistribution of income and wealth in accordance with government policies. They undertake production (but mainly of a different type from corporations), accumulation and final consumption on behalf of the population.

- Households are primarily consumer units, although they may also engage in production (i.e. the operation of unincorporated enterprises and non-profit institutions serving households) and accumulation.

4.2 Grouping transactors with similar objectives and types of behaviour into sectors enhances the usefulness of national accounts for purposes of economic analysis. For such purposes, 2008 SNA defines transactor units, called institutional units, and groups them into institutional sectors and subsectors.

4.3 An institutional unit is defined in 2008 SNA as:

… an economic entity that is capable, in its own right, of owning assets, incurring liabilities and engaging in economic activities and in transactions with other entities.²⁹4.4 An institutional unit is one that is able to:

- own and exchange goods or assets in its own right;

- make economic decisions and engage in economic activities for which it is held directly responsible and accountable at law;

- enter into contracts and incur liabilities on its own behalf; and

- compile, or is able to compile, a complete set of accounts, including a statement of financial position (i.e. a balance sheet of assets and liabilities).

4.5 In some instances, it is statistically advantageous to recognise some entities which do not meet the above criteria as separate institutional units. Notional institutional units are created to enable the collection of their economic activity. These units do not exist as separate institutional units from their owners and therefore are not institutional units in their own right, even where they operate autonomously and keep a full set of accounts.

4.6 2008 SNA identifies two main types of units that may qualify as institutional units: (i) households; and (ii) legal or social entities whose existence is recognised by law or society, independently of the persons or other entities that may own or control them.

Households

4.7 A household is a group of persons who share the same living accommodation, who pool some, or all, of their income and wealth and who consume certain types of goods and services collectively, mainly housing and food. Many assets are owned, or liabilities incurred, jointly by members of the same household, and income received by individual members may be pooled for the benefit of all members. In addition, many expenditure decisions may be made collectively for the household as a whole. As a result of these circumstances, it is not usually possible to draw up meaningful accounts for individual household members. The individual members of multi-person households are therefore not treated as separate institutional units; rather, the household is treated as the institutional unit.

4.8 As well as individual households, there are units described as institutional households that comprise groups of persons staying in hospitals, retirement homes, convents, prisons, etc. for long periods of time.

4.9 An unincorporated enterprise that is entirely owned by one or more members of the same household is treated as a part of that household and not as a separate institutional unit, except when the enterprise is treated as a 'quasi-corporation'.

Legal or social entities

4.10 The second type of institutional unit is a legal or social entity that engages in economic activities and transactions in its own right. 2008 SNA identifies three main types of legal and social entities: corporations, non-profit institutions and government units. In addition, some unincorporated enterprises belonging to households or government units behave in much the same way as corporations and are treated as quasi-corporations when they have complete sets of accounts. In the system, quasi-corporations are treated in the same way as corporations.

4.11 Corporations are defined in 2008 SNA as entities that are:

- capable of generating a profit or other financial gain for their owners;

- recognised at law as separate legal entities from their owners who enjoy limited liability; and

- set up for purposes of engaging in market production.³⁰

4.12 This implies a broader definition than just the legal sense (i.e. legally constituted corporations) as co-operatives, limited liability partnerships, notional resident units and quasi-corporations are also included.

4.13 Legally constituted corporations are created for the purpose of producing goods or services for the market that may be a source of profit or other financial gain to their owners and are collectively owned by shareholders who have the authority to appoint directors responsible for general management.

4.14 Co-operatives are set up by producers for the purposes of marketing their collective output. They effectively operate like corporations; however the profits of such co-operatives are distributed in accordance with their agreed rules and not necessarily in proportion to shares held. Similarly, partnerships whose members enjoy limited liability are separate legal entities that behave like corporations. In effect, the partners are at the same time both shareholders and managers.

4.15 A quasi-corporation is an unincorporated enterprise owned by a resident institutional unit that has sufficient information to compile a complete set of accounts, is operated as if it were a separate corporation and whose de facto relationship to its owner is that of a corporation to its shareholders. Also included is an unincorporated enterprise owned by a non-resident institutional unit that is deemed to be a resident institutional unit because it engages in a significant amount of production in the economic territory over a long or indefinite period of time and is subject to the income tax laws, if any, of the economy in which it is located even if it may have a tax-exempt status. Such a unit is termed a branch in 2008 SNA.

4.16 A notional resident unit is an artificial unit created if a non-resident unit is the legal owner of immovable assets such as land and other natural resources, and buildings and structures. The only exception is made for land and buildings in extra-territorial enclaves of foreign governments such as embassies, consulates, and military bases.

4.17 Two quite different types of units exist that are both often referred to as holding companies. The first is the head office that exercises some aspects of managerial control over its subsidiaries. These may sometimes have noticeably fewer employees, and more at a senior level, than its subsidiaries but it is actively engaged in production. Such units are allocated to the non-financial corporations sector unless all or most of their subsidiaries are financial corporations, in which case they are treated by convention as financial auxiliaries in the financial corporations sector.

4.18 The type of unit properly called a holding company is a unit that holds the assets of subsidiary corporations but does not undertake any management activities. 2008 SNA states that such units should be classified to the financial corporations sector and treated as captive financial institutions and money lenders even if all the subsidiary corporations are non-financial corporations. ASNA deviates from this treatment with holding companies classified to the sector reflective of the major economic activities of the controlled entities.

4.19 Government units are defined in 2008 SNA as unique types of legal entities established by political processes that have legislative, judicial, or executive authority over other institutional units within a defined area. The principal functions of government units are to (i) assume responsibility for provision of goods and services to the community or individual households and to finance their provision out of taxation and other income; (ii) redistribute income and wealth by means of transfers; and (iii) engage in non-market production.

4.20 Government units may engage in productive activity by:

- creating a public corporation whose corporate policy, including pricing and investment, it is able to control;

- creating an NPI that it controls; or

- producing goods or services itself in a unit it owns but that does not exist as a separate legal entity from the government unit.

4.21 Note that the unit in the last example may be treated as a quasi-corporation if the necessary conditions are met; that is, if the unit sets economically significant prices, is operated and managed in a similar way to a corporation and it has a complete set of accounts.

4.22 Non-profit institutions are defined in 2008 SNA as legal or social entities created for the purpose of producing goods or services whose status does not permit them to be a source of income, profit or other financial gain for the units that establish, control or finance them. In practice, their productive activities are bound to generate either surpluses or deficits but any surpluses they happen to make cannot be appropriated by other institutional units. The articles of association by which they are established are drawn up in such a way that the institutional units that control or manage them are not entitled to a share in any profits or other income they generate. For this reason, they are frequently exempted from various kinds of taxes.

4.23 2008 SNA distinguishes two broad types of NPIs: market producers and non-market producers. NPIs are defined to be market producers if they charge prices or fees which have a significant influence on both the amounts producers are willing to supply and the amounts purchasers are willing to buy (i.e. the prices are 'economically significant'). Market NPIs are also defined to include all NPIs serving businesses. Non-market NPIs dispose of their output free of charge, or at prices that are not economically significant. They are classified to the general government sector if controlled by government units. Non-market NPIs that are independent of government are classified to a separate sector in the national accounts. They are called non-profit institutions serving households or NPISHs and are currently classified to the household sector in the ASNA. NPISHs provide goods and services to households free, or at economically insignificant prices.

4.24 In 2008 SNA, institutional units are described as enterprises in their capacity as producers. The term, 'enterprise' may refer to a corporation, a quasi-corporation, an NPI or an unincorporated enterprise. Since corporations and NPIs other than NPISHs are primarily set up to engage in production, the whole of their accounting information relates to production and associated accumulation activities. Government, households and NPISHs necessarily engage in consumption but may also engage in production; indeed, government and NPISHs always engage in production and many, but not all, households do. Whenever the necessary accounting information exists, the production activity of these units is separated from their other activities into a quasi-corporation. It is when this separation is not possible that an unincorporated enterprise exists within the government unit, household or NPISH.

The ASNA equivalent of 2008 SNA institutional units and enterprises

4.25 The units concepts used in the ASNA are based on the ABS Economic Units Model. The ABS uses an economic statistics units model on the ABS Business Register to describe the characteristics of businesses, and the structural relationships between related businesses. The ABS Business Register is used primarily as a register or frame for the various business surveys run by the ABS, and to support the use of administrative data.

4.26 The Australian Business Register (ABR) is the primary source used to identify new businesses. This information flows through to the ABS Business Register. Businesses are included on the ABR when they register with the Australian Taxation Office (ATO) for an Australian Business Number (ABN). The ABN is used as the reference for all dealings between government and business.

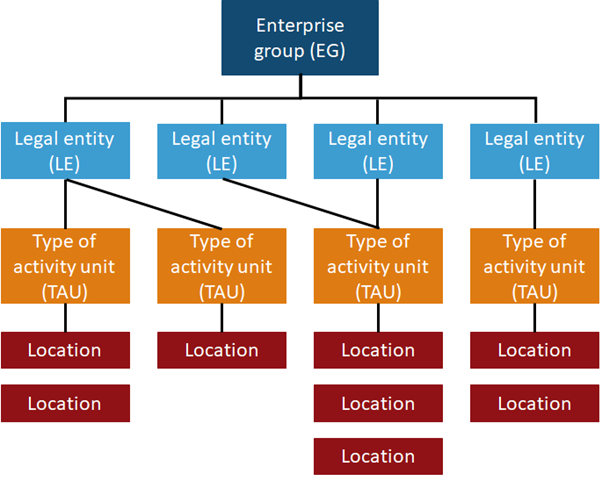

4.27 The units model used by the ABS in determining the structure of businesses is consistent with Australia's Corporations Law and with the definition of institutional units articulated in 2008 SNA. The model consists of the enterprise group (EG), one or more legal entities (LE), one or more type of activity units (TAU), and one or more location units.

4.28 The ABS is unable to actively apply the units model to all ABN registrants. Enterprise groups which are considered sufficiently complex and significant are profiled to create units according to the units model. These groups are known as the profiled population.

4.29 The remainder of ABN registrants are assumed to have simple structures. They are regarded as single legal entity, single enterprise group and TAU. These units are known as the non-profiled population. The two populations are mutually exclusive and cover all organisations in Australia which have registered for an ABN.

4.30 The LE and the TAU are the main institutional and producing units used by the ABS to produce statistical outputs. They do not have a universal relationship with each other, e.g. one to one, one to many, many to one. A variety of relationships exist in some of the larger and more complex Australian enterprise groups. This is a limited departure from the 2008 SNA, which states that there is a hierarchical relationship between institutional and producing units. In the 2008 SNA, the enterprise (the producing view of an individual institutional unit) can be partitioned into one or more establishments. The 2008 SNA statement is true at the EG level, but not necessarily at the LE level.

Figure 4.1 illustrates the nature of the relationships between the unit types in the model. The LE represents the ABN in the diagram as they are usually the same.

Figure 4.1 Illustration of units model used in ASNA

*The legal entity (LE) statistical unit is generally the same as the ABN.

4.32 A legal entity is defined as a unit covering all the operations in Australia of an entity which possesses some or all of the rights and obligations of individual persons or corporations, or which behaves as such in respect of those matters of concern for economic statistics. Examples of legal entities include companies, partnerships, trusts, sole (business) proprietorships, government departments and statutory authorities. Legal entities are institutional units.

4.33 There are some differences between the institutional unit and the practices adopted for the ABS Business Register, even though the legal entity statistical unit is considered to closely approximate the institutional unit as defined in 2008 SNA. The ABS Business Register includes, as legal entity units, individual government departments and authorities and some not-for-profit institutions (e.g. church parishes) that have registered for an ABN but that do not meet the definition for recognition as separate institutional units.

4.34 The ABS Business Register also recognises unincorporated businesses (e.g. sole proprietorships, partnerships, family trusts) that are owned and operated by one or more households and have registered for an ABN as legal entities.

4.35 The enterprise group is an institutional unit covering all the operations in Australia of one or more legal entities under common ownership and/or control. It covers all the operations in Australia of legal entities which are related in terms of the current Corporations Law. These may be legal entities, such as trusts and partnerships, as well as companies. Majority ownership is not required for control to be exercised.

4.36 The type of activity unit is comprised of one or more legal entities, sub-entities or branches of a legal entity that can report productive and employment activities via a set of minimum data items. When defining a TAU, the primary importance is that the activity of the unit be homogeneous. A TAU will be created if accounts sufficient to approximate Industry Value Added (IVA) are available at the ANZSIC subdivision level. Good estimates of accounts are sufficient for this purpose.

4.37 A location is a single, unbroken physical area, occupied by an organisation, at which or from which, the organisation is engaged in productive activity on a relatively permanent basis, or at which the organisation is undertaking capital expenditure with the intention of commencing productive activity on a relatively permanent basis at some time in the future (a location not yet in operation). The exception is the agricultural location unit where land parcels operated as a single property are treated as a single location.

Residence

4.38 The ASNA records the economic activity and wealth of resident institutional units. The residence of each institutional unit is the economic territory with which it has the strongest connection, in other words, its centre of predominant economic interest. This concept is consistent with both 2008 SNA and BPM6. Some key features are as follows:

- the geographic territory under the effective control of the Australia's government;

- any islands belonging to Australia which are subject to the same fiscal and monetary authorities as the mainland;

- the land area, airspace, territorial waters, and continental shelf lying in international waters over which Australia enjoys exclusive rights or over which it has, or claims to have, jurisdiction in respect of the right to fish or to exploit fuels or minerals below the sea bed; and

- territorial enclaves in the rest of the world (that is, geographic territories situated in the rest of the world and used, under international treaties or agreements, by general government agencies of the country). Territorial enclaves include embassies or consulates, military bases, scientific stations, etc. It follows that the economic territory of Australia does not include the territorial enclaves used by foreign governments which are physically located within Australia’s geographical boundaries.

4.39 Specifically, the economic territory of Australia consists of geographic Australia including Cocos (Keeling) Islands and Christmas Island, Norfolk Island, Australian Antarctic Territory, Heard Island and McDonald Islands, Territory of Ashmore Reef and Cartier Island and Coral Sea Islands. However, due to administrative complexities and measurement difficulties, Norfolk Island transactions will not always be captured. Most transactions involving Norfolk Island are not material to Australia's overall economic performance; however, any significant transactions will be identified and included in the relevant statistics.

4.40 An institutional unit has a centre of predominant economic interest in an economic territory when there is a location within the country’s territory from which it engages in economic activities and transactions on a significant scale, on a continuing basis. Such activities are conducted indefinitely or over a longer period of time (generally defined as one year or more). From this definition it follows that short-term production of goods or services undertaken by an Australian enterprise abroad, for example installation of equipment, can be treated as part of the GDP of Australia (and classified as exports of goods or services from Australia).

4.41 In addition, ownership of land or buildings within the economic territory of a country is deemed to give the owner a centre of economic interest in that country. Therefore, all land and buildings are owned by residents. If the centre of predominant economic interest of the non-resident owner of land or buildings remains outside the country where the property is located, the land or buildings are considered to be owned by a foreign direct investment enterprise and controlled by the non-residents. Any rents paid by the tenants of such land or buildings are deemed to be paid to the foreign direct investment enterprise, which in turn makes a transfer of property income to the actual non-resident owner.

4.42 In general, an institutional unit is resident in one and only one economic territory determined by the unit's centre of predominant economic interest. An exception is made for multi-territory enterprises that operate a seamless operation over more than one economic territory; that is, it is run as an indivisible operation with no separate accounts or decisions. Such enterprises are typically involved in cross-border activities and include shipping lines, airlines, hydroelectric schemes on border rivers, pipelines, bridges, tunnels, and undersea cables. If it is not possible to identify a parent or separate branches, it is necessary to prorate the total operations of the enterprise across the individual economic territories.

4.43 Individual members of households who leave the economic territory of a country and return after a limited period (less than one year) continue to be regarded as residents of that country. For example, a member of a resident Australian household who travels abroad for recreation, business, health or other purposes and returns within one year is treated while abroad as a resident of Australia for national accounts (and balance of payments) purposes. In the ASNA, any consumption expenditure undertaken abroad is therefore considered an import of goods or services. An exception to the one-year rule is made in the case of students and medical patients. Students are treated as residents of their country of origin, however long they study abroad. Medical patients abroad are also treated as residents of their country of origin, even if their stay is one year or more.

4.44 Individuals travelling to other countries for seasonal work, and those who cross country borders frequently for work purposes only, also remain residents of their original economic territory. This also applies to locally recruited staff of foreign embassies, consulates, military bases etc., and the crews of ships, aircraft, or other mobile equipment (such as drilling rigs) operating wholly or partly outside the economic territory. The staff of international organisations who work within the enclaves of those organisations are treated as residents of their country of origin if they work for less than one year. If they work with the international organisation for more than one year, they are treated as residents of the host country of the international organisation's enclave.

4.45 Unincorporated enterprises that are not quasi-corporations are not separate institutional units from their owners and, therefore, have the same residence as their owners. Corporations and NPIs are normally expected to have a centre of predominant economic interest in the country in which they are legally constituted and registered. Corporations may be resident in countries different from their shareholders and subsidiary corporations may be resident in countries different from their parent corporations. When a corporation, or unincorporated enterprise, maintains a branch, office or production site in another country in order to engage in production over a long period of time (generally defined as one year or more) but without creating a subsidiary corporation for the purpose, the branch, office or site is considered to be a quasi-corporation (that is, a separate institutional unit) resident in the country in which it is located.

4.46 International organisations established by international agreement (such as the United Nations) are accorded sovereign status, with their own economic territory consisting of the land and structures used by the organisation in the countries where they are physically located. International organisations are therefore not resident units of any country and all transactions with them are treated as transactions with non-residents.

Endnotes

Institutional sectors

4.47 The institutional sectors of 2008 SNA group together similar kinds of institutional units. Corporations, NPIs, government units and households are intrinsically different from each other in that their economic objectives, functions and behaviour are different. Institutional units are allocated to a sector according to the nature of the economic activities they undertake. The three basic economic activities recorded in 2008 SNA are production of goods and services, consumption to satisfy human wants or needs, and accumulation of various forms of capital.

4.48 2008 SNA groups institutional units with similar functions into the following institutional sectors:

- the non-financial corporations sector;

- the financial corporations sector;

- the general government sector;

- the household sector; and

- the non-profit institutions serving households sector.

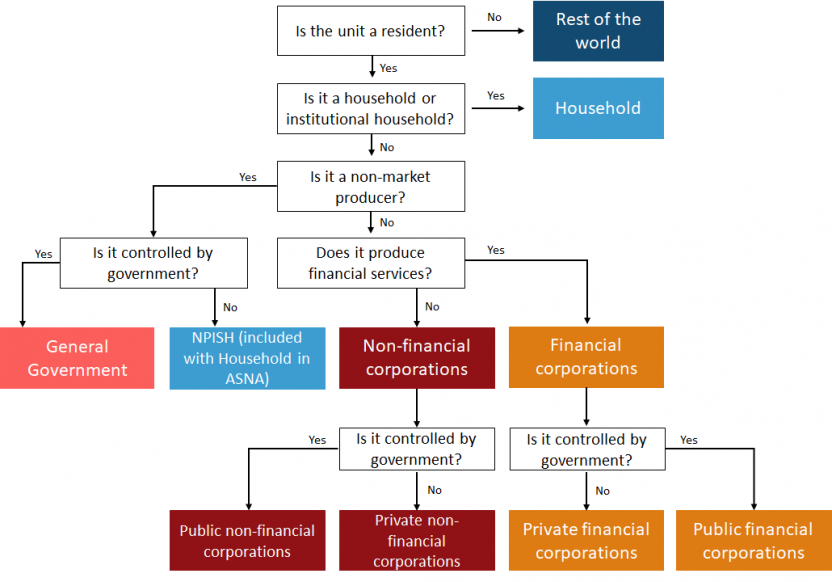

4.49 The figure below shows the 2008 SNA allocation of types of institutional units to institutional sectors. The same allocation rules are followed in the ASNA; however, the NPISH sector is consolidated within the household sector in the Australian System of National Accounts.

Figure 4.2 Illustrative allocation of institutional units to institutional sectors

4.50 The sectors of the total economy and the rest of the world are highlighted. Once non-resident units and households are set aside, only resident legal and social entities remain. Three questions determine the sectoral allocation of all such units. The first is whether the unit is a market or non-market producer. This depends on whether most of the unit’s production is offered at economically significant prices or not.

4.51 The second question determining sectoral allocation applies to non-market units, all of which, including non-market NPIs, are allocated either to general government or to the NPISH sector. The determining factor for sectoral allocation is whether a non-market unit is part of, or controlled by, government.

4.52 The third question determining sectoral allocation applies to market units, all of which, including market NPIs, are allocated to either the non-financial corporations sector or the financial corporations sector.

Non-financial corporations sector

4.53 The non-financial corporations sector consists of all resident corporations, notional institutional units and quasi-corporations that are principally engaged in the production of market goods and/or non-financial services, and holding companies with mainly non-financial corporations as subsidiaries. It includes:

- resident non-financial corporations irrespective of the residence of their shareholders;

- quasi-corporations (including branches of foreign owned non-financial enterprises that are engaged in significant production in the economic territory on a long-term basis);

- non-profit institutions that are market producers of goods or non-financial services; and

- investment funds investing in predominantly non-financial assets such as infrastructure and property.

4.54 2008 SNA identifies three subsectors within the non-financial corporations subsector:

- Public non-financial corporations are resident non-financial corporations or quasi-corporations that are government owned or controlled.

- National private non-financial corporations are resident non-financial corporations or quasi-corporations that are not controlled by government or non-resident institutional units. Market NPIs are included in this subsector.

- Foreign controlled non-financial corporations are resident non-financial corporations or quasi-corporations that are controlled by non-resident institutional units.

4.55 The latter two subsectors are not distinguished in the ASNA. The disaggregation in ASNA is:

- Public non-financial corporations; and

- Private non-financial corporations.

4.56 Public non-financial corporations are further dissected into national and state and local subsectors.

4.57 Private non-financial corporations are further dissected into non-financial investment funds and other private non-financial corporations. The inclusion of non-financial investment funds in the non-financial corporations sector is a departure from 2008 SNA which includes all non-money market investment funds in the financial corporations sector. Non-financial investment funds invest in non-financial assets, usually real estate.

4.58 The ABS publication, Australian National Accounts: Finance and Wealth provides a further sectoral breakdown of non-financial corporations into public and private, with the public sector dissected into national and state and local subsectors, and private sector dissected into non-financial investment funds and other private non-financial corporations.

Financial corporations sector

4.59 The financial corporations sector consists of all resident corporations, notional institutional units, quasi-corporations, and market NPIs that are principally engaged in financial intermediation or in auxiliary financial activities. Financial corporations are distinguished from non-financial corporations because of their different roles in the economy, and the inherent differences in their respective functions and activity. Financial corporations are mainly engaged in financial market transactions, which involve incurring liabilities and acquiring financial assets; that is, borrowing and lending money, providing superannuation, life, health or other insurance, and financial leasing or investing in financial assets. In this process, the corporations are not acting as agents, but rather place themselves at risk by trading in financial markets on their own account. Financial auxiliaries are also classified to the financial corporations sector. They include stockbrokers, insurance brokers, investment advisers, trustees, custodians and nominees, mortgage originators and other entities that are engaged in providing services closely related to financial intermediation, even though they do not intermediate themselves.

4.60 Subsectors of the financial corporations sector identified in ASNA are:

- Central Bank – the Reserve Bank of Australia (RBA).

- Depository corporations – consist of all resident financial corporations and quasi-corporations, except the central bank, that are principally engaged in financial intermediation and have liabilities in the form of deposits or financial instruments that are close substitutes for deposits such as short-term certificates of deposits. This subsector is dissected into:

- Authorised deposit-taking institutions; and

- Other broad money institutions.

- Superannuation funds and insurance corporations – consist of all funds that provide retirement benefits for specific groups of people and all corporations that provide life and other insurance cover, including reinsurance services. This subsector is dissected into:

- Superannuation funds;

- Life insurance corporations; and

- Non-life insurance corporations.

- Financial investment funds – these are collective investment schemes that raise funds by issuing shares or units to the public and the proceeds are invested primarily in financial assets. This subsector is dissected into:

- Money market funds (MMF) – which invest in transferable debt instruments with a residual maturity of no more than one year, bank deposits and instruments that pursue a rate of return that approaches the interest rates of money market instruments; and

- Non-money market financial investment funds (NMMF) – which invest in financial assets other than short-term assets.

- Central Borrowing Authorities (CBAs) – are captive financial institutions established by each State and Territory government to primarily provide finance for public corporations and notional institutional units and other units owned or controlled by the government. They raise funds predominantly by issuing securities, arranging the investment of these unit's surplus funds and participating in the financial management activities of the parent government.

- Securitisers – are financial intermediaries that pool various types of assets such as residential mortgages, commercial property loans and credit card debt, and package them as collateral to issue bonds or short-term debt securities, referred to as asset backed securities.

- Other financial corporations – include other financial intermediaries, financial auxiliaries, money lenders and other captive financial institutions described as follows:

- Other financial intermediaries – includes housing finance schemes established by State and Territory governments; economic development corporations owned by government to fund infrastructure developments;

- Financial auxiliaries – units engaged in activities closely related to financial intermediation, but which do not themselves perform an intermediation role; that is, the auxiliary does not take ownership of the financial assets and liabilities being transacted. The types of corporations included are insurance brokers, loan brokers, investment advisors, managers of superannuation funds, securities brokers, etc.;

- Money lenders – units providing financial services where most of their assets and liabilities are not transacted on the open markets; for example, pawnshops that predominantly engage in lending; and

- Other captive financial institutions – units characterised by having a balance sheet holding financial assets on behalf of other companies. These institutions are usually legal entities such as corporations, trusts or partnerships established for a specific or limited purpose; for example, to hold the assets of a group of subsidiary corporations.

General government sector

4.61 The general government sector consists of government units and non-market NPIs that are controlled by government. The general government sector includes all government departments, offices and other bodies mainly engaged in the production of goods and services outside the normal market mechanism for consumption by government itself and the general public. The units' costs of production are mainly financed from public revenues and they provide goods and services to the general public, or sections of the general public, free of charge or at nominal charges well below costs of production. The sector includes government enterprises mainly engaged in the production of goods and services for other general government units. Also included are NPIs that are serving businesses or households and are composed largely of private sector members but are controlled by governments.

4.62 Subsectors within the general government sector in ASNA are:

- national; and

- state and local.

4.63 Public universities are treated as non-market NPIs controlled by government and are allocated to the general government sector. They are included in the national subsector together with Commonwealth general government.

4.64 Public universities are defined as non-market NPIs based on their funding arrangements. While most public universities were created by State legislation, the bulk of their funding is received from the Commonwealth government. Public universities are allocated to the government sector on the basis that, while no Australian government is able to control universities in the sense of being able to appoint their managing officers, it is clear that the Commonwealth government is able to exercise a significant degree of control through its funding power.

Household sector

4.65 The household sector consists of all resident households, defined as small groups of persons who share accommodation, pool some or all of their income and wealth, and collectively consume goods and services, principally housing and food. Although households are primarily consumers of goods and services, they also engage in other forms of economic activity through their operation of unincorporated enterprises. Such unincorporated enterprises are included in the household sector because the owners of ordinary partnerships and sole proprietorships will frequently combine their business and personal transactions, and complete sets of accounts in respect of the business activity will often not be available.

4.66 The 2008 SNA suggests that the household sector may be divided into subsectors on the basis of the type of income that is the largest source of income for each household or, alternatively, on the basis of other criteria of an economic, socioeconomic or geographical nature. 2008 SNA advises that statistical agencies determine the number and nature of subsectors to suit their own purposes, in view of differing needs across countries in relation to the analysis of the household sector. ASNA does not include any further dissection.

Non-Profit Institutions serving households sector (NPISH)

4.67 All institutional units of a particular type are grouped together within the same sector with the exception of NPIs. They are classified to various sectors depending on the nature of the NPI. Market NPIs are allocated to either the non-financial corporations sector or the financial corporations sector, depending on which sector they serve. Non-market NPIs that are controlled by government units are allocated to the general government sector. For example, an NPI which is mainly financed by government may be controlled by that government. It would not be considered controlled by government if the NPI remains able to determine its policy or programme to a significant extent.³¹ Other non-market NPIs - those not controlled by government - are allocated to the NPISH sector (note again that the NPISH sector has not been separately identified in the ASNA).

4.68 The NPISH sector includes the following two main kinds of NPISHs that provide goods or services to their members or to other households without charge, or at prices that are not economically significant:

- organisations whose primary role is to serve their members, such as trade unions, professional or learned societies, consumers' associations, political parties, churches or religious societies, and social, cultural, recreational and sports clubs; and

- philanthropic organisations, such as charities, relief and aid organisations financed by voluntary transfers in cash, or in kind, from other institutional units.

Rest of the world

4.69 In addition to accounts for the resident sectors, 2008 SNA includes external (rest of the world) accounts, which provide a summary of all transactions of residents with non-residents (e.g. overseas governments, persons and businesses). The rest of the world consists of all non-resident institutional units that enter into transactions with resident units or have other economic links with resident units. It is not a sector for which complete sets of accounts have to be compiled, although it is often convenient to describe the rest of the world as though it were a separate sector.

4.70 As discussed in relation to residence, the rest of the world includes institutional units that may be physically located within the geographical boundary of a country, for example, foreign enclaves such as embassies, consulates or military bases, and international organisations that are not treated as resident institutional units.

Endnotes

Institutional sectors and subsectors in the ASNA

| SECTORS | SUBSECTORS | |

|---|---|---|

| Non-financial corporations | Private | |

| Private non-financial investment funds | ||

| Other private non-financial corporations | ||

| Public | ||

| National | ||

| State and local | ||

| Financial corporations | Central Bank | |

| Depository corporations | ||

| Authorised deposit-taking institutions | ||

| Other broad money institutions | ||

| Superannuation funds and insurance corporations | ||

| Superannuation funds | ||

| Life insurance corporations | ||

| Non-life insurance corporations | ||

| Financial investment funds | ||

| Money market funds | ||

| Non-money market financial investment funds | ||

| Central borrowing authorities | ||

| Securitisers | ||

| Other financial corporations | ||

| General government | National | |

| State and local | ||

| Households (a) | ||

(a) Including uninccorporated businesses n.e.c. and non-profit insitiutions serving households.

4.71 Institutional sector and associated classifications used in ABS statistics are described in the ABS publication, Standard Economic Sector Classifications of Australia (SESCA). The classifications included in SESCA are based on international standards, adapted to suit Australian situations where appropriate. The institutional sector classification, the SISCA, is the main classification used for sectoring in the ASNA. For simplicity of presentation, the SISCA excludes the private/public, level of government and foreign controlled distinctions that are part of the 2008 SNA classification of institutional sectors. These distinctions are contained in other classifications within SESCA. The table above shows the domestic institutional sectors and subsectors included in the ASNA. Accounts for the rest of the world are grouped as 'external accounts' in ASNA. These accounts conform to the 2008 SNA definition of the rest of the world sector.

4.72 With the exception of the combination of the NPISH and household sectors, the ASNA structure corresponds with the structure outlined in 2008 SNA. The subsectors are a combination of 2008 SNA subsectors (adapted to Australian conditions) and other 2008 SNA-compliant classifications from the SESCA, as follows:

- the distinction between the private and public subsectors within the non-financial corporations sector is based on the ABS private/public classification;

- the Commonwealth, state and local, and national subsectors are based on the ABS level of government classification; and

- unlike 2008 SNA, SISCA and the ASNA distinguish authorised deposit-taking institutions from other broad money institutions, CBAs from captive financial institutions, and securitisers from other financial institutions.

4.73 The national subsector is so named because it includes units that are subject to a degree of control from both Commonwealth and state governments, and that cannot be allocated to either a state or Commonwealth subsector. The national subsector therefore includes multi-jurisdictional units in addition to units that are solely under the jurisdiction of the Commonwealth. At present, public universities are the only multi-jurisdictional institutions that are included in the national subsector.

Concordance between ASNA and 2008 SNA sector and subsector definitions

4.74 The composition of the ASNA institutional sectors and subsectors accords with 2008 SNA definitions in most cases. Instances where the ASNA's sectoral composition differs from the 2008 SNA guidelines are described in the following paragraphs.

Non-MMF investment funds

4.75 2008 SNA includes all non-MMF investment funds within the financial corporations sector. However, in ASNA, only those investment funds investing predominantly in financial assets are treated as financial corporations. Those investing in non-financial assets, such as property, are treated as non-financial corporations. This distinction is based on whether the institution's primary income is obtained from rentals, or dividends and interest.

Quasi-corporations in the non-financial and financial corporations sectors

4.76 One feature of both the non-financial corporations sector and the financial corporations sector is that they are designed to cover businesses which are legally, or clearly act as, entities independent of their owners with regard to their income, consumption and capital financing transactions, and accordingly are required to maintain separate profit and loss and balance sheet accounts. Private enterprises classified to these sectors are mainly companies registered under the Companies Act or other Acts of Parliament. However, 2008 SNA also recommends that all quasi-corporations be treated as corporations and allocated either to the non-financial corporations or the financial corporations sector. In Australia, it is often difficult to distinguish quasi-corporations owned by households where the bulk of quasi-corporations are not presently identifiable from ABS data sources. In the ASNA, unincorporated enterprises identified as quasi-corporations are currently limited to large and easily identified enterprises such as partnerships of companies, unit trusts of companies, credit unions, building societies, branches of overseas corporations, and mutual societies. All sole proprietors, partnerships and trusts of individuals are treated as unincorporated enterprises, and are included in the household sector in the ASNA.

Non-profit institutions serving households (NPISH)

4.77 In the ASNA, the recommendations of 2008 SNA are followed with regard to the sector allocation of NPIs that are market producers, and those that are controlled by government units under certain criteria. Contrary to 2008 SNA recommendations, the SISCA does not include separate subsectors within the corporations and general government sectors for NPIs.

4.78 A lack of data availability on the transactions of NPISHs inhibit the construction of a full range of sector accounts for NPISHs. For more information, see the feature article Deconsolidated Household Income Account in the 2013-14 issue of Australian System of National Accounts.