4. The GFS framework

Part A - Introduction

4.1.

The role and responsibilities of government lead government units and public corporations to carry out a variety of activities and functions. The GFS framework organises these economic activities to allow government fiscal activity to be measured and analysed.

4.2.

The GFS framework forms a set of interrelated statements and is designed to facilitate macroeconomic analysis by integrating flows and stock positions. The GFS framework provides the means with which to assess and measure the economic impact of government activity and the liquidity and sustainability of fiscal policy.

4.3.

This chapter describes the GFS framework including the analytical objectives, the structure of the GFS framework, the GFS classifications that comprise the framework, and the related financial statements (outputs).

Part B - The analytical objectives of the GFS framework

4.4.

Paragraph 4.4 of the IMF GFSM 2014 describes the GFS analytical framework as a quantitative tool that supports fiscal analysis. The purpose of the GFS framework is to facilitate the identification, measurement, monitoring, and assessment of the impact of a government’s economic policies, and other activities within the economy.

4.5.

To achieve these objectives, the GFS analytical framework follows the SNA format to enable integrated recording of government economic flows and stocks. The GFS framework requires that the opening values of economic stocks, plus the value of the transactions and other economic flows during the accounting period, should equal the values of the stocks at the end of the accounting period for individual classes of assets and liabilities.

4.6.

In order to provide statistics for each component of the public sector, the GFS framework provides for the identification of the level of government, jurisdiction and institutional sector of each statistical unit in the framework. The GFS framework includes rules that govern the aggregation of data for individual units into totals for each level of government, jurisdiction and sector. The rules provide for the consolidation of flows and stocks that occur between units in the same level of government, jurisdiction or sector.

4.7.

As well as providing the foregoing classification of units by level of government, jurisdiction and sector, the framework provides for the classification of economic flows by type (e.g. transactions versus other economic flows) and function (e.g. general public services, public order and safety, etc.) and economic stocks by type. At the broadest level, flows are subdivided between transactions and other economic flows. Transactions are categorised by type as either revenues, expenses, net acquisition of non-financial assets, net acquisition of financial assets, net incurrence of liabilities or net contributions of capital. Stocks are subdivided by type between non-financial assets, financial assets, liabilities, and shares and other contributed capital. Each of the classifications is hierarchical, such that each of the broad categories is disaggregated into subcategories, which in turn are further broken down into classes. The degree of disaggregation varies from category to category and is designed to cater for all analytical requirements.

4.8.

The GFS framework presents information about opening stocks, flows during the accounting period and closing stocks, which enables the derivation of key analytical aggregates to support fiscal analysis. The key analytical aggregates that are derived from component statements are:

- GFS Net Operating Balance - this is the difference between GFS revenues and GFS expenses. It reflects the sustainability of government operations and is also known as the change in net worth due to transactions.

- GFS Net Lending (+) / Borrowing (-) - this shows the financing requirements of government, indicating the extent to which government is either putting financial resources at the disposal of other sectors in the economy or abroad, or utilising the financial resources generated by other sectors in the economy or from abroad. It is calculated as the GFS Net Operating Balance less the net acquisition of non-financial assets. A positive result reflects a net lending position and a negative result reflects a net borrowing position. This is also known as the change in net financial worth due to transactions.

- GFS Net Worth - this is the total stock of assets minus liabilities and shares / contributed capital. For the general government sector, net worth is assets less liabilities since shares and contributed capital is zero. It is an economic measure of wealth and reflects the contribution of governments to the wealth of Australia.

- GFS Net Financial Worth - this is the total stock of financial assets minus liabilities and shares/contributed capital. For the general government sector, net financial worth is financial assets less liabilities since shares and contributed capital is zero. It is an economic measure of the stock position of financial assets owned by the government of Australia.

- Cash Surplus (+) / Deficit (-) - this is the net cash inflow from operating activities minus net cash outflow from investments in non-financial assets. The cash surplus/deficit is a measure of a sector's cash flow requirements and if positive (i.e. a surplus), it reflects cash available to governments to either increase financial assets or decrease liabilities. When this measure is negative (i.e. a deficit), it identifies the extent to which a government needs to run down its financial assets in order to finance the cash shortfall.

4.9.

The GFS framework provides a structure within which very detailed presentations of GFS can be formulated. In theory, the items in each of the basic statements can be disaggregated to the finest levels of each of the stocks and flows classifications and cross-classified according to the level of government, jurisdiction and sector of each unit in the framework. In practice, there are practical and quality limits to the degree of detail that can be tabulated. However, the previously discussed objectives of the framework are readily achieved with this design.

Part C - The structure of the GFS framework

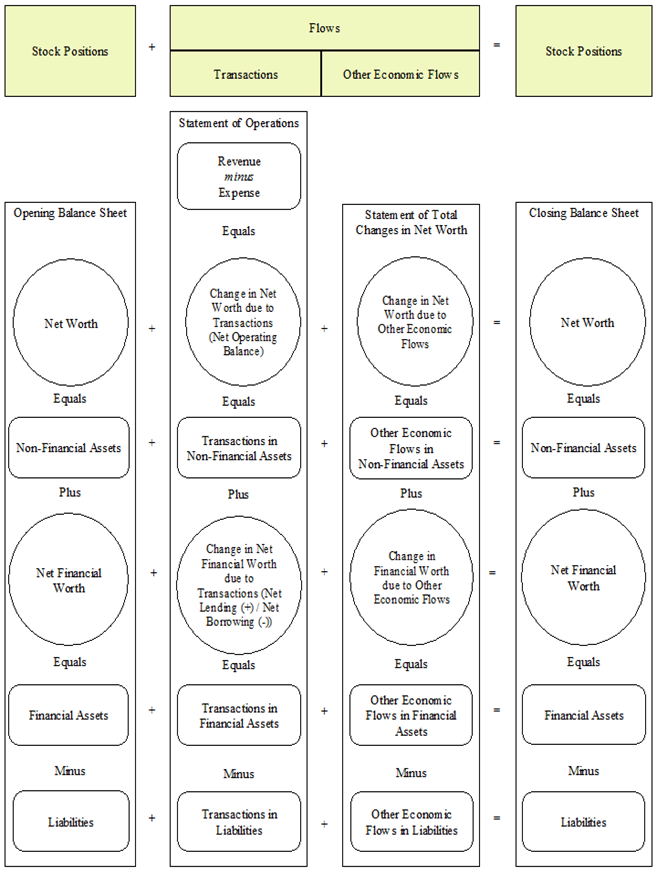

4.10.

The GFS framework combines elements from the GFS balance sheet, statement of operations, the statement of sources and uses of cash, and statement of stocks and flows to describe and record economic events that occur during an accounting period. This can be shown through the maintenance of opening stock figures, details of the transactions and other economic flows that occur during the accounting period, and closing stock figures. The relationships between stocks and flows can be analysed to explain the effects of government policy and the fiscal effects of government operations.

4.11.

The GFS analytical framework in diagram 4.1 presents the accrual component of the broader GFS framework and the relationships between the elements within it. In the broadest sense, the GFS analytical framework illustrates that during the accounting period, the closing stock position equals the opening stock position plus transactions and other economic flows.

Diagram 4.1 - The GFS analytical framework

Source: International Monetary Fund Government Finance Statistics Manual, 2014.

4.12.

The key analytical aggregates are shown in circles in the broad GFS analytical framework in Diagram 4.1. They are:

- Net worth with both opening and closing balances represented;

- Change in net worth due to transactions which is equal to the net operating balance;

- Change in net worth due to other economic flows;

- Net financial worth with both opening and closing balances represented;

- Change in net financial worth due to transactions which is equal to net lending (+) / net borrowing (-); and

- Change in net financial worth due to other economic flows

4.13.

Please note that the cash surplus (+) / cash deficit (-) is also a key analytical aggregate in the broader GFS framework, although this does not appear in the analytical framework diagram. The GFS cash surplus (+) / cash deficit (-) is represented by cash flows from operating activities plus cash flows from investments in non-financial assets.

4.14.

The second analytical aggregate in the statement of operations is the GFS net lending(+) / net borrowing(- ). This is derived as the net operating balance less net acquisition of non-financial assets. GFS net lending(+) / net borrowing(-) is also equal to the net acquisition of all financial assets arising from transactions minus the net incurrence of all liabilities arising from transactions. This can be demonstrated arithmetically as follows in Table 4.1:

| (1) | Net Lending (+) / Net Borrowing (-) | = | Net Operating Balance | - | Net Change in Non-Financial Assets due to Transactions | ||

|---|---|---|---|---|---|---|---|

| (2) | Net Operating Balance | = | Change in Net Worth due to Transactions | ||||

| (3) | Change in Net Worth due to Transactions | = | Net Change in Non-Financial Assets due to Transactions | + | Net Change in Financial Assets / Liabilities due to Transactions* | ||

| Therefore: | |||||||

| (4) | Net Operating Balance | = | Net Change in Non-Financial Assets due to Transactions | + | Net Change in Financial Assets / Liabilities due to Transactions* | ||

| And substituting in (1) | |||||||

| (5) | Net Lending (+) / Net Borrowing (-) | = | Net Change in NonFinancial Assets due to Transactions | + | Net Change in Financial Assets / Liabilities due to Transactions | - | Net Change in Non-Financial Assets due to Transactions |

| Therefore: | |||||||

| (6) | Net Lending (+) / Net Borrowing (-) | = | Net Change in Financial Assets / Liabilities due to Transactions | ||||

Note: Also known as the Change in Net Financial Worth or GFS Net lending (+) / Net Borrowing.

Part D - GFS classifications

4.15.

In order for the GFS analytical framework to provide the means with which to assess and measure the impact of government policies and other activity on the Australian economy, financial data must enter the framework. The data that feed through the GFS analytical framework are primarily sourced from the financial accounts of state and territory treasuries, the Department of Finance, local governments and universities. These data are classified to the GFS analytical framework through a range of GFS classifications. The data are then processed and aggregated by the ABS to identify the key GFS analytical balances. For more information on the sources of GFS data and methods of compilation, please see Chapter 14 of this manual.

4.16.

The GFS framework provides for the classification of units by level of government (LOG), jurisdiction (JUR), and institutional sector (INST). It also provides for the economic classification of stocks and flows by type (economic type classification, or ETF), and selected economic flows by function (classification of the functions of government - Australia, or COFOG-A). The COFOG-A replaces the government purpose classification (GPC) breakdown previously used. Each of the classifications are hierarchical in nature and are disaggregated into various subcategories. The degree of disaggregation varies from category to category, and is designed to cater for all analytical requirements. For further information on the classification of units see Chapter 2 and Appendix 1 Part A.

Unit classifications

4.17.

The main GFS classifications applied to units are the level of government (LOG), jurisdiction (JUR), and institutional sector (INST) classifications (for definitions, see Chapter 2 of this manual). Also used is the Australian and New Zealand Standard Industrial Classification, 2006 (or ANZSIC).

4.18.

Unit classifications are first determined at the time a unit comes into the coverage of GFS. This usually happens when a unit is created by a government in Australia, or when an existing unit is split to more than one unit or is combined with another unit to form a new unit. Once determined, unit classifications are reviewed only when major changes occur to the functions and / or operating environment of the unit.

4.19.

The GFS unit classification process involves examining Acts of Parliaments (where applicable) and the unit’s financial statements (i.e. the income and expenditure (profit and loss) statement, balance sheet, and cash flow statement). This process is intended to disclose the range of activities in which the unit engages, and the legislative background to its creation. Such information is used to determine whether the unit qualifies as a separate institutional unit in it's own right, and whether it falls within the scope of GFS. The information (supplemented where necessary by information obtained directly from the unit), is used to determine the classification(s) applicable to the unit. Further information on the classification of units and sectors may be found in Chapter 2 of this manual.

Flows and stocks classifications and frameworks

4.20.

The GFS flows and stocks classifications and frameworks may be viewed from two perspectives, an input perspective and an output perspective. The input perspective takes into account the nature and structure of the data that enter the framework. The main sources of GFS data are government accounts, which provide accounting data that have to be reclassified and reorganised on an economic basis to be suitable for conversion to statistical output. As well, the input perspective identifies flows and stocks (e.g. those subject to consolidation) that do not enter final output as such. The output perspective views the classifications almost entirely (plus additional derived items) as the lists of items that appear in published statistics. The detailed classifications are set out in Appendix 1 Part A, Part B, and Part C of this manual.

4.21.

The main flows and stocks classifications in GFS are the:

- Economic type framework (ETF);

- Source destination classification (SDC);

- Type of asset and liability classification (TALC);

- Taxes classification (TC); and

- Classification of the functions of government - Australia (COFOG-A).

Economic type framework (ETF)

4.22.

The economic type framework (ETF) is the primary framework that is used to classify flows and stocks according to their economic nature (e.g. revenues, expenses, transactions in financial assets and liabilities, transactions in non-financial assets, assets, liabilities) in GFS. The structure of the ETF is hierarchical, and consists of a 1-digit level (division), a 2-digit level (subdivision), a 3-digit level (group) and a 4-digit level (class). The divisions reflect the primary financial statements of the government at the broadest level and the subdivisions describe the major components that form part of each financial statement. Each group and class details the assets, liabilities, revenues and expenses which comprise each subdivision. The full classification can be found in Appendix 1 Part A and Part B of this manual. The divisions and subdivisions are shown in Table 4.2 below and include the following:

| ETF | Descriptor | |

|---|---|---|

| 1 | Revenue and expenses | |

| 11 | Revenue | |

| 12 | Expenses | |

| 2 | Statement of sources and uses of cash | |

| 21 | Cash flows from operating activities | |

| 22 | Cash flows from transactions in non-financial assets | |

| 23 | Cash flows from transactions in financial assets for policy purposes | |

| 24 | Cash flows from investments in financial assets for liquidity management purposes | |

| 25 | Cash flows from financing activities | |

| 26 | Increase / (decrease) in cash held | |

| 3 | Transactions in financial assets and liabilities | |

| 31 | Transactions in financial assets (net) | |

| 32 | Transactions in liabilities (net) | |

| 4 | Transactions in non-financial assets | |

| 41 | Acquisitions of non-financial assets | |

| 42 | Disposals of non-financial assets | |

| 5 | Other economic flows of assets and liabilities | |

| 51 | Holding gains and losses (revaluations) | |

| 52 | Other changes in volume | |

| 6 | Intra-unit transfers | |

| 60 | Intra-unit transfers | |

| 7 | Supplementary information | |

| 71 | Memorandum items - balance sheet | |

| 72 | Contingent liabilities | |

| 73 | Provisions for doubtful debts | |

| 74 | Debt maturity | |

| 75 | Salary sacrifice expenses | |

| 76 | Own-account capital formation | |

| 8 | Balance sheet | |

| 81 | Fixed produced assets | |

| 82 | Other produced assets | |

| 83 | Non-produced assets | |

| 84 | Financial assets | |

| 85 | Liabilities | |

| 86 | Net worth | |

Revenue and expenses (ETF 1)

4.23.

Revenue (ETF 11) records public sector revenue in the form of taxation revenue (ETF 111); sales of goods and services (ETF 112); property income (ETF 113); other current revenue (ETF 114); and capital revenue (ETF 115). The finer level detail of each of these elements is further discussed in Chapter 6 of this manual.

4.24.

Expense (ETF 12) records public sector expenses in the form of superannuation expenses (ETF 121); other employee expenses (ETF 122); non-employee expenses (ETF 123); depreciation (ETF 124); current transfer expenses (ETF 125); capital transfer expenses (ETF 126); interest expenses (ETF 127); and other property expenses (ETF 128). The finer level detail of each of these elements is further discussed in Chapter 7 of this manual.

The statement of sources and uses of cash (ETF 2)

4.25.

Cash flows from operating activities (ETF 21) record cash flows in the form of cash receipts from operating activities (ETF 211); cash payments for employee expenses (ETF 212); and cash payments for non-employee expenses (ETF 213). The finer level detail of each of these elements is further discussed in Chapter 12 of this manual.

4.26.

Cash flows from transactions in non-financial assets (ETF 22) records cash flows in the form of expenditure on non-financial assets (net) (ETF 221). The finer level detail of this element is further discussed in Chapter 12 of this manual.

4.27.

Cash flows from transactions in financial assets for policy purposes (ETF 23) records cash flows in the form of advances paid (net) (ETF 231); and equity acquisitions, disposals, and sale of equity (net) (ETF 232). The finer level detail of each of these elements is further discussed in Chapter 12 of this manual.

4.28.

Cash flows from investments in financial assets for liquidity management purposes (ETF 24) records cash flows in the form of increase in investments (ETF 241). The finer level detail of this element is further discussed in Chapter 12 of this manual.

4.29.

Cash flows from other financing activities (ETF 25) records cash flows in the form of advances received (net) (ETF 251); borrowing (net) (ETF 252); deposits received (ETF 253); and other financing (net) (ETF 259). The finer level detail of each of these elements is further discussed in Chapter 12 of this manual.

4.30.

Increase / (decrease) in cash held (ETF 26) records cash flows in the form of increase / (decrease) in cash held (ETF 261). The finer level detail of this element is further discussed in Chapter 12 of this manual.

Transactions in financial assets and liabilities (ETF 3)

4.31.

Transactions in financial assets (net) (ETF 31) records transactions in the form of transactions in financial assets (net) (ETF 311). The finer level detail of this element is further discussed in Chapter 8 and Chapter 10 of this manual.

4.32.

Transactions in liabilities (net) (ETF 32) records transactions in the form of transactions in liabilities (net) (ETF 321). The finer level detail of this element is further discussed in Chapter 8 and Chapter 10 of this manual.

Transactions in non-financial assets (ETF 4)

4.33.

Acquisitions of non-financial assets (ETF 41) records transactions in the form of acquisitions of nonfinancial assets (ETF 411). The finer level detail of this element is further discussed in Chapter 8 and Chapter 9 of this manual.

4.34.

Disposals of non-financial assets (ETF 42) records transactions in the form of disposals of non-financial assets (ETF 421). The finer level detail of this element is further discussed in Chapter 8 and Chapter 9 of this manual.

Other economic flows of assets and liabilities (ETF 5)

4.35.

Holding gains and losses (revaluations) (ETF 51) record the value of other economic flows in the form of holding gains and losses (revaluations) (ETF 511). The finer level detail of this element is further discussed in Chapter 11 of this manual.

4.36.

Other changes in volume (ETF 52) record the value of other economic flows in the form of other changes in volume (ETF 521). The finer level detail of this element is further discussed in Chapter 11 of this manual.

Intra-unit transfers (ETF 6)

4.37

Intra-unit transfers (ETF 60) records intra-unit transfers other than holding gains and losses and accrued transactions. This classification is used exclusively by the ABS for the processing of GFS data. Further information on this item may be found in Appendix 1 Part B of this manual.

Supplementary information (ETF 7)

4.38.

Memorandum items - balance sheet (ETF 71) records supplementary information relating to the GFS balance sheet in the form of implicit transfers (ETF 711); liabilities in arrears and related charges (ETF 712); and non-performing loans (ETF 713). The finer level detail of each of these elements is further discussed in Appendix 1 Part B of this manual.

4.39.

Contingent liabilities (ETF 72) records supplementary information relating to the GFS balance sheet in the form of explicit contingent liabilities (ETF 721); and implicit contingent liabilities (ETF 722). The finer level detail of each of these elements is further discussed in Appendix 1 Part B of this manual.

4.40.

Provisions for doubtful debts (ETF 73) records provisions for anticipated doubtful debts during the reporting period. Provisions for doubtful debts are not recognised in GFS, but are recorded in the AGFS15 as part of the supplementary information so that the ABS can derive the face value of financial assets and liabilities which is required for international statistical reporting. Provisions or allowances for doubtful debts are not included in GFS output, and accounts receivable in the balance sheet is recorded gross of such provisions or allowances. Provisions for doubtful debts are further discussed in Chapter 13 Part A, and Appendix 1 Part A of this manual.

4.41.

Debt maturity (ETF 74) records the value of public sector debt in the form of debt by maturity valued at market value (ETF 741). The finer level detail of this element is further discussed in Appendix 1 Part B of this manual.

4.42.

Salary sacrifice expenses (ETF 75) records the value of the benefits supplied by a public sector employer to employees under a salary sacrifice arrangement. The finer level detail of this element is further discussed in Appendix 1 Part B of this manual.

4.43.

Own-account capital formation (ETF 76) records the value of own-account capital formation in the form of own-account superannuation payments (ETF 761); own-account employee payments other than superannuation (ETF 762); and own-account non-employee payments (ETF 763). The finer level detail of each of these elements is further discussed in Appendix 1 Part B of this manual.

Balance sheet (ETF 8)

4.44.

The balance sheet records the value of assets in the form of fixed produced assets (ETF 81); other produced assets (ETF 82); non-produced assets (ETF 83); and financial assets (ETF 84). The finer level detail of these categories is further discussed in Chapter 8, Chapter 9, and Chapter 10 of this manual.

4.45.

Liabilities (ETF 85) record the value of the liabilities of public sector units. The finer level detail of this category is further discussed in Chapter 8, Chapter 9, and Chapter 10 of this manual.

4.46.

Net worth (ETF 86) records the residual of the value of government assets minus government liabilities in the form of net worth (ETF 8611). The finer level detail of this element is further discussed in Chapter 8, Chapter 9, and Chapter 10 of this manual.

Source destination classification (SDC)

4.47.

The source destination classification (SDC) is a classification that is used for the identification of the sectors that are the source and destination of transactions in, and stocks of, financial assets and liabilities in the Australian GFS. It is also used to identify the sectors that are the source and destination of transactions in non-financial assets. In addition, the SDC identifies the source of the funds if a transaction is an operating revenue or a cash receipt, and the destination of the funds if the transaction is an operating expense or a cash payment.

4.48.

The SDC specifically identifies:

- the institutional sector and level of government of the unit against which the financial claim represented by the asset / liability is held for transactions in, and stocks of, financial assets and liabilities;

- the institutional sector and level of government of the unit which acquires a non-financial asset or which disposes of a non-financial asset; and

- the institutional sector and level of government (where applicable) of the unit (including nongovernment units) from which revenues are receivable (the source) or to which expenses are payable (the destination) for each transaction.

4.49.

The SDC classifications are shown below in Table 4.3 as:

| SDC | Descriptor |

|---|---|

| 110 | Commonwealth public non-financial corporations |

| 120 | Commonwealth public financial corporations |

| 130 | Commonwealth general government |

| 21j | State / territory public non-financial corporations |

| 22j | State / territory public financial corporations |

| 23j | State / territory general government |

| 31j | Local public non-financial corporations |

| 32j | Local public financial corporations |

| 33j | Local general government |

| 41j | Control not further defined public non-financial corporations |

| 42j | Control not further defined public financial corporations |

| 43j | Control not further defined general government |

| 911 | Resident private non-financial corporations |

| 912 | Resident private depository corporations |

| 913 | Resident households |

| 914 | Resident non-profit institutions serving households |

| 915 | Other resident private financial corporations |

| 919 | Residents not elsewhere classified |

| 921 | Non-resident private depository corporations |

| 929 | Non-residents not elsewhere classified |

Note: j denotes the state / territory of jurisdiction.

4.50.

The public sector (SDC 100 - 43j) comprises Commonwealth public non-financial corporations, Commonwealth public financial corporations, and Commonwealth general government units (SDC 110, SDC 120, and SDC 130); State / territory public non-financial corporations, State / territory public financial corporations, and State / territory general government units (SDC 21j, SDC 22j, and SDC 23j) which are further disaggregated by state of jurisdiction; Local public non-financial corporations, Local public financial corporations, and Local general government units (SDC 31j, SDC 32j, and SDC 33j) which are further disaggregated by state of jurisdiction; and Control not further defined public non-financial corporations, Control not further defined public financial corporations, and Control not further defined general government units (SDC 41j, SDC 42j, and SDC 43j) which are further disaggregated by state of jurisdiction. Control not further defined units are made up of public universities and other units that are not controlled by any one particular jurisdiction in Australia.

4.51.

The non-public sector consists of resident units which comprise resident private non-financial corporations (SDC 911), resident private depository corporations (SDC 912), resident households (SDC 913), resident non-profit institutions serving households (SDC 914), other resident private financial corporations (SDC 915), and residents not elsewhere classified (SDC 919).

4.52.

The non-public sector also consists of non-resident units which comprise non-resident private depository corporations (SDC 921) and non-residents not elsewhere classified (SDC 929).

Type of asset and liability classification (TALC)

4.53.

The type of asset and liability classification (TALC) is a classification used for the identification of nonfinancial and financial assets and liabilities for GFS output purposes. The structure of the TALC is hierarchical, and consists of a 1-digit level (division), a 2-digit level (group) and a 3-digit level (class). The division distinguishes between government non-financial assets and financial assets or liabilities, the group reflects the type of non-financial asset, financial asset or liability at a broad level and the class reflects the details of the individual assets and liabilities which comprise each group. Further information on the TALC can be found in Chapter 8, Chapter 9, Chapter 10 and Appendix 1 Part A of this manual. The division and group levels of the TALC are shown in Table 4.4 below:

| TALC | Descriptor | |

|---|---|---|

| Non-Financial Assets | ||

| 1 | Fixed Produced assets | |

| 11 | Buildings and structures | |

| 12 | Machinery and equipment | |

| 13 | Cultivated biological resources | |

| 14 | Intellectual property products | |

| 2 | Other produced assets | |

| 21 | Inventories | |

| 22 | Valuables | |

| 23 | Other produced assets | |

| 3 | Non-produced assets | |

| 31 | Tangible non-produced assets | |

| 32 | Intangible non-produced assets | |

| 33 | Other non-produced assets | |

| Financial Assets and Liabilities | ||

| 4 | Financial assets | |

| 41 | Currency and deposits | |

| 42 | Securities and related assets | |

| 43 | Loans and placements | |

| 44 | Insurance, superannuation and standardised guarantee schemes | |

| 45 | Other financial assets | |

| 5 | Liabilities | |

| 51 | Currency and deposits | |

| 52 | Securities and related liabilities | |

| 53 | Loans and placements | |

| 54 | Insurance, superannuation and standardised guarantee schemes | |

| 55 | Other liabilities | |

4.54.

Buildings and structures (TALC 11) record public sector holdings of fixed produced assets in the form of buildings and structures. These comprise dwellings (TALC 111); buildings other than dwellings (TALC 112); land improvements (TALC 113); and other structures not elsewhere classified (TALC 119).

4.55.

Machinery and equipment (TALC 12) record public sector holdings of fixed produced assets in the form of machinery and equipment. These comprise transport equipment (TALC 121); information, computer and telecommunications equipment (TALC 122); and other machinery and equipment not elsewhere classified (TALC 129).

4.56.

Cultivated biological resources (TALC 13) record public sector holdings of fixed produced assets in the form of cultivated biological resources. These comprise animal resources yielding repeat products (TALC 131); and tree, crop, and plant resources yielding repeat products (TALC 132).

4.57.

Intellectual property products (TALC 14) record public sector holdings of fixed produced assets in the form of intellectual property products. These comprise research and development (TALC 141); mineral exploration and evaluation (TALC 142); computer software (TALC 143); databases (TALC 144); entertainment, literary and artistic originals (TALC 145); and intellectual property products not elsewhere classified (TALC 149).

4.58.

Weapons systems (TALC 15) record public sector holdings of fixed produced assets in the form of weapons systems. This comprises weapons systems (TALC 151).

4.59.

Inventories (TALC 21) record public sector holdings of other produced assets in the form of inventories. These comprise inventories - materials and supplies (TALC 211); inventories - work in progress (TALC 212); inventories - finished goods (TALC 213); inventories - goods for resale (TALC 214); and military inventories (TALC 215).

4.60.

Valuables (TALC 22) record public sector holdings of other produced assets in the form of valuables. These comprise valuables (TALC 221).

4.61.

Other produced assets (TALC 23) records public sector holdings of other produced assets. These comprise other not elsewhere classified produced assets (TALC 239).

4.62.

Tangible non-produced assets (TALC 31) record public sector holdings of non-produced assets in the form of tangible non-produced assets. These comprise land (TALC 311); mineral and energy resources (TALC 312); non-cultivated biological resources (TALC 313); water resources (TALC 314); radio spectra (TALC 315); and tangible non-produced assets not elsewhere classified (TALC 319).

4.63.

Intangible non-produced assets (TALC 32) record public sector holdings of non-produced assets in the form of intangible non-produced assets. These comprise marketable operating leases (TALC 321); permits to use natural resources (TALC 322); permits to undertake specified activities (TALC 323); entitlement to future goods and services on an exclusive basis (TALC 324); goodwill and marketing assets (TALC 325); and intangible non-produced assets not elsewhere classified (TALC 329).

4.64.

Other non-produced assets (TALC 33) record public sector holdings of other non-produced assets. These comprise other non-produced assets not elsewhere classified (TALC 339).

4.65.

Currency and deposits (TALC 41 and TALC 51) record public sector holdings of currency and deposit financial assets and liabilities. These comprise cash and deposits (TALC 411 and TALC 511); Special drawing rights (SDRs) (TALC 412 and TALC 512); and monetary gold (bullion) (TALC 414 asset only), and monetary gold (allocated and unallocated) (TALC 414 and TALC 511).

4.66.

Securities and related assets / liabilities (TALC 42 and TALC 52) record public sector holdings of financial assets and liabilities in debt securities and related items. These comprise debt securities (TALC 421 and TALC 521); financial derivatives (TALC 422 and TALC 522); employee stock options (TALC 423 and TALC 523); equity including contributed capital (TALC 424 and TALC 524); and investment fund shares or units (TALC 425 and TALC 525).

4.67.

Loans and placements (TALC 43 and TALC 53) record public sector holdings of loan and placements in the form of financial assets and liabilities. These comprise financial leases (TALC 431 and TALC 531); advances - concessional loans (TALC 432 and TALC 532); advances other than concessional loans (TALC 433 and TALC 533); and loans and placements not elsewhere classified (TALC 439 and TALC 539).

4.68.

Insurance, superannuation and standardised guarantee schemes (TALC 44 and TALC 54) record public sector holdings of financial assets and liabilities in insurance, superannuation, and standardised guarantee schemes. These comprise non-life insurance technical reserves (TALC 441 and TALC 541); life insurance and annuities entitlements (TALC 442 and TALC 542); provisions for defined benefit superannuation (TALC 443 and TALC 543); claims of superannuation funds on superannuation manager (TALC 444 and TALC 544); and provisions for calls under standardised guarantee schemes (TALC 445 and TALC 545).

4.69.

Other financial assets (TALC 45) and other liabilities (TALC 55) record public sector holdings of other financial assets and liabilities. These comprise provisions for employee entitlements other than superannuation (TALC 451 and TALC 551); accounts receivable (TALC 452) / accounts payable (TALC 552); and other financial assets not elsewhere classified (TALC 459) / other liabilities not elsewhere classified (TALC 559).

Taxes classification (TC)

4.70.

The taxes classification (TC) is a classification used for the identification of taxation revenue by type of tax, and is used for output purposes in the Australian GFS. The structure of the TC is hierarchical, and consists of a 1-digit level (division), a 2-digit level (group) and a 3-digit level (class). The division reflects the different types of taxes at the broad level; the group and class provide further detail about the taxes that comprise each division. The full classification of the TC can be found in Chapter 6 and Appendix 1 Part A of this manual. The division and group levels of the TC are shown in Table 4.6 below:

| TC | Descriptor | |

|---|---|---|

| 1 | Taxes on income, profits and capital gains | |

| 11 | Income and capital gains taxes levied on individuals | |

| 12 | Income and capital gains taxes levied on enterprises | |

| 13 | Income taxes levied on non-residents | |

| 2 | Taxes on employers' payroll and labour force | |

| 21 | Taxes on employers' payroll and labour force | |

| 3 | Taxes on property | |

| 31 | Taxes on immovable property | |

| 32 | Estate, inheritance and gift taxes | |

| 4 | Taxes on provision of goods and services | |

| 41 | General taxes on provision of goods and services | |

| 42 | Excises | |

| 43 | Taxes on international trade | |

| 44 | Taxes on gambling | |

| 45 | Taxes on insurance | |

| 46 | Taxes on financial and capital transactions | |

| 5 | Taxes on the use of goods and performance of activities | |

| 51 | Motor vehicle taxes | |

| 52 | Franchise taxes | |

| 53 | Other taxes on the use of goods and performance of activities | |

4.71.

Income and capital gains taxes levied on individuals (TC 11) records taxes on income, profits, and capital gains in the form of income and capital gains taxes levied on individuals. These comprise personal income tax (TC 111); government health insurance levy (TC 112); mining withholding tax (TC 113); capital gains tax on individuals (TC 114); prescribed payments by individuals (TC 115); fringe benefits tax (TC 116); and other income tax levied on individuals (TC 119).

4.72.

Income and capital gains taxes levied on enterprises (TC 12) records taxes on income, profits, and capital gains in the form of income and capital gains taxes levied on enterprises. These comprise company income tax (TC 121); income tax paid by superannuation funds (TC 122); capital gains taxes on enterprises (TC 123); and prescribed payments by enterprises (TC 124).

4.73.

Income taxes levied on non-residents (TC 13) records taxes on income, profits, and capital gains in the form of income taxes levied on non-residents. These comprise dividend withholding tax (TC 131); interest withholding tax (TC 132); and income taxes levied on non-residents not elsewhere classified (TC 139).

4.74.

Taxes on employer's payroll and labour force (TC 21) records taxes on employers' payroll and labour force. This comprises payroll taxes (TC 211), superannuation guarantee charge (TC 212), and taxes on employers' payroll and labour force not elsewhere classified (TC 219).

4.75.

Taxes on immovable property (TC 31) records taxes on property in the form of taxes on immovable property. These comprise land taxes (TC 311); municipal rates (TC 312); metropolitan improvement rates (TC 313); property owners' contributions to fire brigades (TC 314); and taxes on immovable property not elsewhere classified (TC 319).

4.76.

Estate, inheritance and gift taxes (TC 32) records taxes on property in the form of estate, inheritance, and gift taxes. These comprise estate, inheritance, and gift taxes (TC 321).

4.77.

General taxes on provision of goods and services (TC 41) records taxes on provision of goods and services in the form of general taxes on provision of goods and services. These comprise sales tax (TC 411); and goods and services tax (GST) (TC 412).

4.78.

Excises (TC 42) records taxes on provision of goods and services in the form of excises. These comprise excises on crude oil, LPG and petroleum products (TC 421); excises on beer and potable spirits (TC 422); excises on tobacco products (TC 423); Excise Act duties not elsewhere classified and refunds of Excise Act duties (TC 424); agricultural production taxes (TC 425); and levies on statutory corporations (TC 426).

4.79.

Taxes on international trade (TC 43) records taxes on provision of goods and services in the form of taxes on international trade. These comprise customs duties on imports (TC 431); customs duties on exports (TC 432); and agricultural produce export taxes (TC 433).

4.80.

Taxes on gambling (TC 44) records taxes on provision of goods and services in the form of taxes on gambling. These comprise taxes on government lotteries (TC 441); taxes on private lotteries (TC 442); taxes on gambling devices (TC 443); casino taxes (TC 444); race betting taxes (TC 445); and taxes on gambling not elsewhere classified (TC 449).

4.81.

Taxes on insurance (TC 45) records taxes on provision of goods and services in the form of taxes on insurance. These comprise insurance companies' contributions to fire brigades (TC 451); third party insurance taxes (TC 452); and taxes on insurance not elsewhere classified (TC 459).

4.82.

Taxes on financial and capital transactions (TC 46) records taxes on provision of goods and services in the form of taxes on financial and capital transactions. These comprise financial institutions transactions taxes (TC 461); government borrowing guarantee levies (TC 462); stamp duties on conveyances (TC 463); stamp duties on shares and marketable securities (TC 464); and other stamp duties on financial and capital transactions (TC 465).

4.83.

Motor vehicle taxes (TC 51) records taxes on the use of goods and performance of activities in the form of motor vehicle taxes. These comprise stamp duty on vehicle registration (TC 511); road transport and maintenance taxes (TC 512); heavy vehicle registration fees and taxes (TC 513); and other vehicle registration fees and taxes (TC 519).

4.84.

Franchise taxes (TC 52) records taxes on the use of goods and performance of activities in the form of franchise taxes. These comprise gas franchise taxes (TC 521); petroleum products franchise taxes (TC 522); tobacco franchise taxes (TC 523); and liquor franchise taxes (TC 524).

4.85.

Other taxes on the use of goods and performance of activities (TC 53) records other taxes on the use of goods and performance of activities. These comprise broadcasting station licences (TC 531); television station licences (TC 532); departure tax (TC 533); clean energy and related taxes (TC 534); taxes on the use of goods and performance of activities levied on non-residents (TC 535); and other taxes on the use of goods and performance of activities not elsewhere classified (TC 539).

The classification of the functions of government - Australia (COFOG-A)

4.86.

The classification of the functions of government - Australia (COFOG-A) (formerly known as the government purpose classification (GPC)) is used to classify selected revenues, all expenses, and all transactions in non-financial assets in terms of the government purpose (e.g. health, education, defence) of the expenditure. The COFOG-A is based on the 2008 SNA Classification of the Functions of Government (COFOG). For further information on the COFOG-A, see Appendix 1 Part C of this manual.

4.87.

The COFOG-A is grouped according to type of government function or purpose. The structure of the COFOG-A is hierarchical and consists of a 2-digit level (division), a 3-digit level (group) and a 4-digit level (class). The divisions reflect the broad objectives of government; the groups and classes detail the means by which these broad objectives are achieved. The full classification can be found in Appendix 1 Part C of this manual. The divisions are shown in Table 4.7 below and include the following:

| COFOG-A | Descriptor |

|---|---|

| 01 | General public services |

| 02 | Defence |

| 03 | Public order and safety |

| 04 | Economic affairs |

| 05 | Environmental protection |

| 06 | Housing and community amenities |

| 07 | Health |

| 08 | Recreation, culture and religion |

| 09 | Education |

| 10 | Social protection |

| 11 | Transport |

4.88.

General public services (COFOG-A 01) include transactions from executive and legislative organs; financial and fiscal affairs; external affairs; foreign economic aid; general services; basic research; research and development on general public services; general public services not elsewhere classified, public debt transactions; and transfers of a general character between different levels of government.

4.89.

Defence (COFOG-A 02) includes transactions from military and civil defence; foreign military aid; research and development on defence; and defence not elsewhere classified.

4.90.

Public order and safety (COFOG-A 03) includes transactions from police services; fire protection services; law courts and associated activities; prisons; research and development on public order and safety; and public order and safety not elsewhere classified.

4.91.

Economic affairs (COFOG-A 04) includes transactions from general and economic affairs, commercial, and labour affairs; agriculture, forestry, fishing and hunting; fuel and energy; mining, manufacturing and construction; communication; other industries; research and development on economic affairs; and economic affairs not elsewhere classified.

4.92.

Environmental protection (COFOG-A 05) includes transactions from waste management; waste water management; pollution abatement; protection of biodiversity and landscape; research and development on environmental protection; and environmental protection not elsewhere classified.

4.93.

Housing and community amenities (COFOG-A 06) includes transactions from housing development; community development; water supply; street lighting; research and development on housing and community amenities; and housing and community amenities not elsewhere classified.

4.94.

Health (COFOG-A 07) includes transactions from medical products, appliances and equipment; outpatient services; hospital services; mental health institutions; community health services; public health services; research and development on health; and health not elsewhere classified.

4.95.

Recreation, culture and religion (COFOG-A 08) includes transactions from recreational and sporting services; cultural services; broadcasting, publishing and film production services; religious and other community services; research and development on recreation, culture and religion; and recreation, culture and religion not elsewhere classified.

4.96.

Education (COFOG-A 09) includes transactions from pre-primary and primary education; secondary education; tertiary education; education not definable by level; subsidiary services to education; research and development on education; and education not elsewhere classified.

4.97.

Social protection (COFOG-A 10) includes transactions from sickness and disability; old age; survivors; family and children; unemployment; housing; social exclusion not elsewhere classified; research and development on social protection; and social protection not elsewhere classified.

4.98.

Transport (COFOG-A 11) includes transactions from road transport; bus transport; water transport; railway transport; air transport; multi-mode urban transport; pipeline and other transport; research and development on transport and transport not elsewhere classified.

Part E - Financial statements relating to the GFS framework

4.99.

There are four key output statements in the broader GFS framework. Each is made up of financial data from the Department of Finance, state and territory treasuries, local governments, universities, and control not further defined units that contain data classified by relevant classifications in the GFS framework. The primary financial statements relating to the GFS analytical framework are the:

- Statement of operations - this statement (formerly known as the GFS operating statement) records GFS revenues, GFS expenses, and the net acquisition of non-financial assets.

- Statement of sources and uses of cash - this statement (formerly known as the Cash Flow Statement) records cash inflows and outflows during the accounting period.

- Balance sheet - this statement records the stock positions of government assets, liabilities and equity.

- Statement of stocks and flows - this statement records the opening stocks of assets and liabilities, the transactions in these, the value of holding gains and losses (revaluations) and other volume changes, and the closing stocks of assets and liabilities.

4.100.

The statement of operations (formerly known as the GFS operating statement) is a summary of the transactions (except transactions in financial assets and liabilities) of a sector or subsector in a given reporting period. It records transactions that increase or decrease net worth such as revenues and expenses, the net investment in non-financial assets, the net acquisition of financial assets, and the net incurrence of liabilities during the reporting period. This statement also facilitates the derivation of key GFS derived items such as the net operating balance and the net lending (+) / net borrowing (-) position, net acquisition of non-financial assets and gross fixed capital formation. The GFS data items that make up the statement of operations are further discussed in Chapter 5 of this manual.

4.101.

The statement of sources and uses of cash (formerly known as the cash flow statement) records cash inflows and outflows during the reporting period.

4.102.

The balance sheet records the stock positions of assets, liabilities and the net worth of the sector or subsector at the end of the reporting period. The classification of assets and liabilities is further discussed in Chapter 8, Chapter 9 and Chapter 10 of this manual.

4.103.

The statement of stocks and flows records the opening stocks, transactions, revaluations, other volume changes and closing stocks of assets and liabilities, and contains three analytical items, GFS net worth, net debt and net financial worth.

The statement of operations

4.104.

The statement of operations records transactions in revenue, expenses, and non-financial assets. Transactions are classified according to whether they increase net worth (revenue), decrease net worth (expense), or change the stocks of non-financial assets. A broad outline of the statement of operations is given in Table 4.8 below, and the full details can be found in Chapter 5 of this manual.

| GFS Revenue |

| Less |

| GFS Expense |

| Equals |

| GFS Net Operating Balance |

|---|

| Less |

| Net Acquisition of Non-Financial Assets |

| Equals |

| GFS Net Lending (+) / Net Borrowing (-) |

4.105.

The GFS statement of operations includes two balancing items. The first of these is the net operating balance (NOB) which is used to measure the fiscal effects of government operations, and is derived as total revenue less total expenses. Revenues and expenses are increases or decreases in GFS net worth resulting from transactions. Certain exchange transactions, such as the acquisition of non-financial produced assets for cash, do not change net worth but simply change the composition of assets, liabilities or equity. The net operating balance is equal to the change in net worth due to transactions.

4.106.

The net operating balance is measured as revenue minus expense (other than depreciation ETF 124). The gross operating balance may be used if depreciation is unknown. However, the net operating balance is preferred because it captures all of the cost of government operations during the reporting period.

4.107.

The second analytical balance in the GFS statement of operations is the GFS net lending (+) / net borrowing (-). This measures the public sector's financing requirements and is derived as the net operating balance less transactions in non-financial assets. The GFS net lending (+) / net borrowing (-) is equal to the change in net financial worth due to transactions. The GFS statement of operations is further discussed in Chapter 5 of this manual.

The statement of sources and uses of cash

4.108.

The statement of sources and uses of cash (formerly known as the cash flow statement in Australian GFS) records the net cash inflows from government operating activities, the net increase / (decrease) in cash held and the GFS cash surplus / cash deficit. The statement of sources and uses of cash records when cash is received by the government and cash is paid by the government during an accounting period and is important for assessing the liquidity of the general government and public sectors.

4.109.

Paragraph 4.34 of the IMF GFSM 2014 recommends that statistics on cash-based monetary flows should reflect transactions as close to the payment stage as possible. In GFS, the cash-based data recorded in the statement of sources and uses of cash are complementary to the data in the accrual GFS statements and form an integral part of the complete GFS framework. Table 4.9 below shows a broad outline of the elements that make up the GFS statement of sources and uses of cash.

| Cash receipts from operating activities |

| Less |

| Cash payments for employee expenses |

| Less |

| Cash payments for non-employee expenses |

| Equals |

| Cash flows from operating activities |

|---|

| Plus |

| Cash flows from transactions in non-financial assets |

| Plus |

| Cash flows from transactions in financial assets for policy purposes |

| Plus |

| Cash flows from investments in financial assets for liquidity management purposes |

| Plus |

| Cash flows from other financing activities |

| Equals |

| Increase (+) / decrease (-) in cash held |

| Cash flows from operating activities plus net cash flows from transactions in non-financial assets |

| Equals |

| GFS Cash Surplus (+) / GFS Cash Deficit (-) |

4.110.

The cash flows from operating activities is a net measure representing the cash receipts arising from operating activities less cash payments arising from operating activities. Operating activities in this context indicates the types of activities that are recorded in the statement of operations. Cash flows from operating activities include cash receipts from taxation, sales of goods and services, grants and subsidies, property income, and all other revenue earning activities recorded in the statement of operations. The item also includes cash payments for employee expenses, including cash contributions to superannuation schemes, purchases of goods and services, and payment of subsidies and grants, current and capital transfers, property expenses and all other expense-incurring activities recorded in the statement of operations.

4.111.

The GFS cash surplus (+) / GFS cash deficit (-) reflects the level of cash available to governments to either increase financial assets or decrease liabilities. When GFS cash surplus (+) / GFS cash deficit (-) is positive, it indicates there are additional cash funds resulting from the net cash inflow from operating activities and the cash outflow from own account capital formation and investment in other non-financial assets. This residual value reflects the cash available to governments to either increase financial assets or decrease liabilities.

4.112.

When GFS cash surplus (+) / GFS cash deficit (-) is negative, it indicates that there is a shortage of residual cash funds as a result from the net cash inflow from operating activities and the cash outflow from investment in non-financial assets. This identifies the extent to which a government needs to run down its financial assets or borrow in order to finance the cash shortfall.

4.113.

The net cash flows from other financing activities is a net measure representing the cash flows from advances received, borrowing, deposits received, and other financing.

4.114.

The net change in the stock of cash measures the change in the stock of cash by adding the cash surplus (+) / cash deficit (-) to the net cash inflows from financing activities.

4.115.

The statement of sources and uses of cash is further discussed in Chapter 12 of this manual.

The balance sheet

4.116.

The balance sheet records the stock positions of assets and liabilities at the beginning of a reporting period and at the end of a reporting period. The balancing item of the balance sheet is GFS net worth which represents the total value of assets minus the total value of liabilities. Table 4.10 shows a broad outline of the elements that make up the GFS balance sheet.

| Balance sheet item | Opening Balance Sheet | Closing Balance Sheet |

|---|---|---|

| Non-Financial Assets | xx | xx |

| Plus | ||

| Financial Assets | xx | xx |

| Less | ||

| Liabilities | xx | xx |

| = | ||

| GFS Net Worth | xx | xx |

4.117.

The assets that are included in the GFS balance sheet are economic assets. These are defined as resources over which ownership rights are enforced by institutional units and from which economic benefits may be derived by holding them, or using them over a period of time. Assets that are not owned and controlled by a reporting unit or sector, and assets that have no economic value are excluded from the balance sheet. In the GFS balance sheet, assets are recorded as either non-financial assets or financial assets.

4.118.

Non-financial assets are all economic assets other than financial assets. Non-financial assets comprise all of the elements in the type of asset and liability classification (TALC) that classifies non-financial assets (TALC 1, 2 and 3). These include non-financial fixed produced assets in the form of buildings and structures (TALC 11); machinery and equipment (TALC 12); cultivated biological resources (TALC 13); intellectual property products (TALC 14) and weapons systems (TALC 15). Also included as non-financial assets are other non-financial produced assets in the form of inventories (TALC 21); valuables (TALC 22); and other produced assets (TALC 23). Further included as non-financial assets are non-financial non-produced assets in the form of tangible non-produced assets (TALC 31); intangible non-produced assets (TALC 32) and other non-produced assets (TALC 33).

4.119.

Financial assets are assets in the form of financial claims on other economic units. They are the counterparts of the liabilities of the units on which the claims are held (except in the case of monetary gold) and so are often referred to together in GFS. Financial assets comprise all of the elements in the type of asset and liability classification (TALC) that classifies financial assets (TALC 4). These include currency and deposits (TALC 41); securities and related assets (TALC 42); loans and placements (TALC 43); insurance, superannuation and standardised guarantee schemes (TALC 44); and other financial assets (TALC 45).

4.120.

Liabilities are defined as the obligation to provide funds or other resources of economic value to another unit. Liabilities are the counterparts of financial assets in GFS (with the exception of monetary gold in the form of gold bullion held as reserves). Liabilities comprise all of the elements in the type of asset and liability classification (TALC) that classifies liabilities (TALC 5). These include currency and deposits (TALC 51); securities and related liabilities (TALC 52); loans and placements (TALC 53); insurance, superannuation, and standardised guarantee schemes (TALC 54); and other liabilities (TALC 55).

4.121.

The GFS balance sheet also contains several memorandum items. These record additional information of analytic interest on specific items for GFS purposes. Memorandum items in GFS differ to those in commercial accounting in that they are mandatory rather than optional. The memorandum items to the GFS balance sheet are recorded as part of the supplementary information in GFS, and include implicit transfers (ETF 711); liabilities in arrears and related charges (ETF 712); and non-performing loans (ETF 713). Memorandum items are further discussed in Appendix 1 Part B of this manual.

4.122.

Further discussion on the GFS balance sheet and the elements that comprise it can be found in Chapter 8, Chapter 9, Chapter 10, Chapter 15, and Appendix 1 Part A of this manual.

The statement of stocks and flows

4.123.

As with the GFS balance sheet (see Chapter 8 of this manual), the statement of stocks and flows records assets and liabilities and GFS net worth. However, the statement of stocks and flows also records the opening stocks, transactions, revaluations, other volume changes and closing stocks of the assets and liabilities, with the analytical items shown as GFS net worth, net debt and net financial worth. Table 4.11 shows a broad outline of the elements that make up the GFS statement of stocks and flows.

| Balance sheet item | Opening Stocks | Transactions | Revaluations | Other Volume Changes | Closing Stocks | |

|---|---|---|---|---|---|---|

| Assets | ||||||

| Non-financial assets | xx | xx | xx | xx | xx | |

| Financial assets | xx | xx | xx | xx | xx | |

| Total assets | xx | xx | xx | xx | xx | |

| Less | ||||||

| Liabilities | xx | xx | xx | xx | xx | |

| Equals | ||||||

| GFS net worth | xx | xx | xx | xx | xx | |

| Plus | ||||||

| Net debt | xx | xx | xx | xx | xx | |

| Equals | ||||||

| Net financial worth | xx | xx | xx | xx | xx | |

4.124.

In parallel to the GFS balance sheet, the assets that are included in the statement of stocks and flows are recorded as either financial assets or non-financial assets. Financial assets are assets in the form of financial claims on other economic units, and they appear in the statement of stocks and flows as currency and deposits; advances paid; investments, loans and placements; other non-equity assets; equity; and other financial assets. In GFS, financial assets are the counterparts of the liabilities of the units on which the claims are held (for further information (see Chapter 8 and Chapter 10 of this manual for further information).

4.125.

Non-financial assets are all assets other than financial assets, and they appear in the statement of stocks and flows as non-financial produced assets, inventories, valuables, land, other non-produced assets, and other non-financial assets (see Chapter 8 and Chapter 9 of this manual for further information).

4.126.

The liabilities recorded in the statement of stocks and flows include deposits held, advances received; borrowing; unfunded superannuation and other employee entitlements; and other non-equity liabilities (see Chapter 8 and Chapter 10 of this manual for further information).

4.127.

Also recorded as part of the statement of stocks and flows are net debt and net financial worth. Further detail of the elements that make up the statement of stocks and flows may be found in Chapter 15 of this manual.

Other statements in GFS

4.128.

There are six other output statements in GFS whose compilation is required for international statistical reporting purposes, and are published as output by the ABS. These are:

- The statement of total changes in net worth;

- The statement of contingent liabilities;

- The statement of stocks and flows of financial assets and liabilities by source; and

- Gross public sector debt and other liabilities at market value by level of government subsector;

- Net public sector debt and other liabilities at market value by level of government subsector; and

- The presentation of debt instruments by market value by maturity.

4.129.

The statement of total changes in net worth combines elements of the statement of operations and the statement of stocks and flows in the one statement, and serves to highlight the total changes in net worth of government. Paragraph 4.46 of the IMF GFSM 2014 notes that the statement of total changes in net worth provides a clear statistical explanation of the factors causing the change in the net worth of government. It explains the sources of changes in assets and liabilities from one reporting period to another in terms of transactions in revenue and expense and other economic flows. For further information please see Chapter 15 of this manual.

4.130.

The summary statement of explicit contingent liabilities and net implicit obligations for future social security benefits records explicit contingent liabilities such as one-off guarantees, and implicit contingent liabilities such as the present value of implicit obligations for future social security benefits in the one statement. In this context, social security benefits relate to the international concept of the social security schemes. At the time of writing, there are no such social security schemes in Australia. For further information please see Chapter 15 of this manual.

4.131.

The classification of stocks and flows by financial asset and liabilities by source records the opening stocks of financial assets and liabilities, the transactions, holding gains and losses (revaluations), other economic flows and the closing stocks. In this classification, financial assets and liabilities are split into domestic and foreign financial assets / liabilities and whether these are bank or non-bank items. The ABS records the classification of stocks and flows by financial asset and liabilities by source as an indicator of default risk. For further information please see Chapter 15 of this manual.

4.132.

Gross public sector debt and other liabilities at market value by level of government subsector records debt instruments at their current market value, and by level of government subsector on the gross basis. In this statement, the market value debt instruments are recorded for the Commonwealth general government, total general government sector, total public non-financial sector and total public financial sector on the gross basis. For further information please see Chapter 15 of this manual.

4.133.

Net public sector debt and other liabilities at market value by level of government subsector records debt instruments at their current market value, and by level of government subsector on the net basis. In this statement, the market value debt instruments are recorded for the Commonwealth general government, total general government sector, total public non-financial sector and total public financial sector on the net basis. For further information please see Chapter 15 of this manual.

4.134.

The presentation of debt instruments at market value by maturity records government debt instruments at market value into:

- Short term debt by original maturity;

- Long term debt by original maturity - with payment due in one year or less;

- Long term debt by original maturity - with payment due in more that one year (long term debt by remaining maturity); and

- Short term debt by remaining maturity.

4.135.

The ABS records debt instruments at market value by maturity to provide data that assists in managing liquidity risk. For further information please see Chapter 15 of this manual.