- Repetto, R., Magrath, W., Wells, M., Beer, C. and F. Rossini (1989) Wasting Assets: Natural Resources in the National Income Accounts. Washington, DC: World Resources Institute.

This is not the latest release View the latest release

Environmental-economic accounts

Australian System of National Accounts: Concepts, Sources and Methods

Reference period

2020-21 financial year

Released

9/07/2021

Introduction

23.210 This section describes the notion of environmental-economic accounts and the underpinnings of the environmental-economic accounts produced by the ABS. Those accounts follow the recommendations of the United Nations' System of Environmental-Economic Accounting (SEEA). The SEEA is an international statistical standard that had its genesis as a satellite system of the SNA. As a result, the SEEA utilises concepts, structures and methods that are largely consistent with those used in the SNA, allowing the SEEA to integrate environmental and economic information within a single framework.

23.211 Over the past 50 years, macroeconomic policy has largely been based on information flowing from the SNA framework and the aggregates it produces. However, gross domestic product and national income fail to capture many vital aspects of national wealth and well-being, such as changes in quality of health, extent of education, social connection, political voice, unpaid household work, and changes in quality and quantity of natural resources. Further, GDP actually includes ''defensive expenditures'' such as spending on household security, health and environmental protection. This is because the SNA measures activity within ''the market''.

23.212 It is well understood that much of what maintains and enhances well-being occurs outside the market. For example, environmental goods and services are considered 'non-market' within the SNA, and well within the production boundary. They are implicitly superabundant, free inputs to production. As a result, they are used as inputs to production, but not charged as costs of production; in effect:

23.213 A country could exhaust its mineral resources, cut down its forests, erode its soil, pollute its aquifers, and hunt its wildlife to extinction, but measured income would not be affected as these assets disappeared.¹¹⁷

23.214 A key limitation of the economic information system is that it cannot answer some of the higher order questions policymakers (and society) are asking. In particular, it does not appropriately describe the relationship between the environment and economy.

23.215 Therefore, a comprehensive analysis of environmental issues, and the policy responses to deal with these, must be informed by socio-economic information about drivers, pressures, impacts and responses. This information should be integrated with the associated bio-physical information so that relationships and linkages can be properly understood.

23.216 Environmental-economic accounts provide a conceptual framework for integrating the environmental and economic information systems. Similarly, organising environmental and economic information into an accounting framework has the capacity to improve basic statistics, and allows for the calculation of indicators which are precisely defined, consistent and interlinked, as illustrated in the figure below:

Figure 23.1 The information pyramid

Image

Description

This image in an information pyramid that is split into three layers. Basic data (economic and environmental) forms the bottom layer. Next layer up is the Accounts (SEEA) which allow for the top layer of the pyramid, Indicators, to be calculated.

Endnotes

The System of Integrated Environmental and Economic Accounting

23.217 The conceptual model adopted by the ABS and the international statistical community for environmental accounts is the United Nations' System of Environmental-Economic Accounting (SEEA). SEEA was endorsed by the United Nations Statistical Commission as an international standard in February 2012. The structures, concepts and classifications used in the SEEA are consistent with those used in the SNA, meaning that accounts produced under the SEEA support the bringing together of environmental and economic information within a common framework. This allows for consistent analysis of the contribution of the environment to the economy, the impact of the economy on the environment, and the efficiency of the use of environmental resources within the economy.

23.218 The SEEA framework, like the SNA, utilises flow and stock accounts containing estimates expressed in both physical and monetary terms. More broadly, the SEEA utilises the following four types of accounts:

- Physical flow accounts record flows of natural inputs from the environment to the economy, flows of products within the economy and flows of residuals generated by the economy. These flows include water and energy used in production (e.g. of agricultural commodities) and waste flows to the environment (e.g. solid waste to landfill).

- Functional accounts for environmental transactions record the many transactions between different economic units (i.e. enterprises, households and governments) that concern the environment. Functional accounts may explicitly identify environmentally-related transactions contained within standard SNA accounts (such flows are not explicitly shown within typical SNA presentations). For example, Environmental Protection Expenditure (EPE) accounts disaggregate traditional national accounting flows to reveal those monetary transactions relevant to environmental protection.

- Asset accounts in physical and monetary terms measure the natural resources available and changes in the amount available. Asset accounts focus on the key individual components of the environment: mineral and energy resources; timber resources; fish/aquatic resources; other biological resources; soil resources; water resources; and land. They include measures of the stock of each environmental asset at the beginning and end of an accounting period and record the various changes in the stock due to extraction, natural growth, discovery, catastrophic loss or other reasons.

The compilation of asset accounts in physical terms can provide valuable information on resource availability

and may help in the assessment of sustainability. A particular feature of the SEEA asset accounts is the

estimation of depletion of natural resources in physical and monetary terms. For non-renewable resources the

quantity of depletion is equal to the quantity of resource extracted but for renewable resources the quantity of

depletion must consider the underlying population, its size, rate of growth and associated sustainable yield.

- The SEEA Central Framework is complemented by two other publications: namely, SEEA Ecosystem Accounting (SEEA EA) and SEEA Applications and Extensions. In terms of the former, ecosystem accounts are a relatively new and developing field. The United Nations Statistical Commission, in March 2021, adopted chapters 1-7 of the System of Environmental-Economic Accounting—Ecosystem Accounting (SEEA EA) as an international statistical standard. In the same document, chapters 8-11 present internationally recognised statistical principles and recommendations for valuation of ecosystem services and assets. The SEEA Ecosystem Accounting (SEEA EA) constitutes an integrated and comprehensive statistical framework for organising data about habitats and landscapes, measuring the ecosystem services, tracking changes in ecosystem assets, and linking this information to economic and other human activity.Ecosystems are areas containing a dynamic complex of plant, animal and micro-organism communities and their non-living environment interacting as a functional unit. Ecosystem accounts are structured to summarise information about these areas, their changing capacity to operate as a functional unit, and their delivery of benefits to humanity.

- The benefits received by humanity are known as ecosystem services. They are delivered in different forms and are grouped into three broad categories:

- provisioning services – the benefits received from the natural inputs provided by the environment such as water, timber, fish and energy resources;

- regulatory services – the benefits provided when an ecosystem operates as a sink for emissions and other residuals, when an ecosystem provides flood mitigation services or when an ecosystem provides pollination services to agriculture; and

- cultural services – the benefits provided when an ecosystem such as a forest, provides recreational, spiritual or other benefits to people.

23.219 Each of the different types of accounts is connected within the SEEA framework but each one focuses on a different part of the interaction between the economy and the environment. Examples of the relationships between the different accounts include:

- Asset accounts and ecosystem accounts focus on the stock and changes in the stock of environmental assets, with asset accounts focusing on the individual components and ecosystem accounts focusing on the interactions within and between these components.

- Changes in the stock are often the result of economic activity which in turn is the focus of physical flow accounts. Measurement of flows of natural inputs in the physical supply and use tables is consistent with the measurement of extraction in the asset accounts and the measurement of provisioning services in ecosystem accounts.

- Measurement of flows of residuals to the environment as recorded in physical supply and use tables is an important consideration in the measurement of ecosystem services, particularly regulatory services.

- Measures of the flows of natural inputs and residuals can also be related to transactions recorded in functional accounts for environmental protection and resource management, including investment in cleaner technologies and flows of environmental taxes and subsidies. For example, payments for emission permits recorded in functional accounts can be related to the flows of emissions recorded in the physical supply and use tables and to the operating surplus of emitters and final expenditures by households.

- The effectiveness of the expenditure for environmental purposes may, ultimately, be assessed by changes in the capacity of ecosystems to continue their delivery of ecosystem services as recorded in ecosystem accounts.

23.220 These examples serve to highlight the many and varied relationships between the accounts, each taking a different perspective. These relationships are supported using common concepts, definitions and classifications throughout the SEEA.

Valuation

23.221 One of the most challenging aspects of environmental-economic decision-making is obtaining appropriate information to inform trade-offs between the environmental assets that deliver a range of non-market goods and services, including ecosystem services, against development alternatives for which there are clearly defined economic values. The SNA and the SEEA Central Framework include the value of environmental assets that have direct economic values. For example, land, timber, minerals and energy resources are included in the national balance sheet in the Australian System of National Accounts.

23.222 The preferred valuation in the SNA and the SEEA Central Framework is based on market transactions. Some environmental assets (and many ecosystem services) are not transacted in markets; in these instances, non-market valuation techniques must be used. For example, mineral deposits are owned by the Commonwealth and state governments in Australia, and are not sold on active markets; rather, they are extracted under a mining lease arrangement. Under these circumstances, it is recommended that the value of the mineral deposit be calculated as the net present value of future expected income resulting from the extraction of this mineral deposit.

23.223 In some cases, the value of certain ecosystem services may be included in the value of goods and services traded in markets. For example, the value of pollination is captured in the value of agricultural crop production, while tourism operators derive income from the people visiting natural attractions such as Uluru and the Great Barrier Reef.

23.224 The development of standardised methods for identifying and separately distinguishing the value of environmental assets and ecosystem services is an on-going area of work in the SEEA. The recognition of the value of these assets and services potentially provides important information to decision-makers; for example, in informing comparisons between various development alternatives.

Integrating the environmental and economic information systems

23.225 A comprehensive national environmental information system should be built on two pillars:

- the essential bio-physical information pertaining to the state of the environment; and

- the complementary socio-economic information on drivers, pressures, impacts and responses.

23.226 The pillars should be 'integrated' to ensure that the bio-physical and socio-economic dimensions of environmental issues can be considered concurrently in policy formulation and in other decision making. Integration is achieved by the use of common frameworks, classifications and standards. The information in each pillar should be organised so that, for each environmental domain of interest, users could seamlessly move from the bio-physical aspects to the socio-economic aspects and vice versa.

23.227 This implies that there should be a common logic for organising both the bio-physical and socio-economic information. Such logic could be built around the various environmental domains (e.g. water, air, land) organised in a driver-pressure-state-impact-response (DPSIR) framework – as depicted in Figure 23.2 below. The integration of information would also ensure that environmental issues that cut across domains, such as biodiversity and greenhouse gas emissions can be appropriately analysed.

Figure 23.2 The DPSIR framework

The image illustrates the driver-pressure-state-impact-response (DPSIR) framework. It describes the interactions between society (Socio-economic) and environment (Biophysical). The flow chart starts with Driver and then flows onto Pressure. Next is a flow to State, then a flow to Impact and finally to Response. Flows from Response can be to any of the previous four items.

23.228 The physical stores of information could be disparate, with the expectation that much of the bio-physical information would be stored by agencies such as the Bureau of Meteorology (BoM) and much of the socio-economic information would be stored by the ABS. However, the information for both pillars would be locatable and accessed through a single portal. From a user perspective, there would be a single virtual information system, although the source of particular information sets would be clearly identifiable within this system.

23.229 To develop such a virtual information system and to achieve integration, the ABS, BoM and other agencies would work in partnership. This would involve working together on relevant frameworks, standards and classifications, as well as the underlying logic for organising environmental information, including determining appropriate metadata requirements. Developing and maintaining the portal would be a joint responsibility of the contributing agencies.

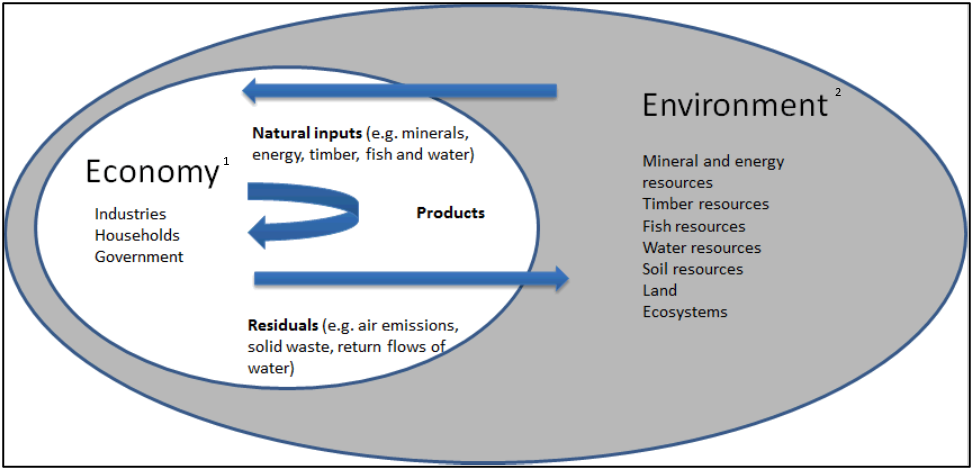

23.230 Figure 23.3 below illustrates the domain that integrated environmental-economic accounts seek to inform – in particular, it is the interaction between the economy and the environment that is the focus of our information framework. The figure further describes the various agencies engaged in integrating environmental and economic information systems, and the location of their primary institutional responsibilities.

Figure 23.3 Integrating information systems - Primary institutional responsibilities

The image illustrates the domain that integrated environmental-economic accounts seek to inform. It shows the interaction between the economy and the environment.

Listed under Economy are: Industries, Households, and Government.

Listed under Environment are: Mineral and energy resources, Timber resources, Fish resources, Water resources, Soil resources, Land, and Ecosystems.

The image shows that Residuals (e.g. air emissions, solid waste, return flows of water) flow from the economy to the environment.

Natural inputs (e.g minerals, energy, timber, fish and water) flow from the environment to the economy.

Products are produced by the economy.

- Australian Bureau of Statistics; Australian Bureau of Agricultural and Resource Economics and Sciences; Department of Climate Change, Energy, the Environment and Water; Department of Prime Minister and Cabinet; Productivity Commission; Treasury; state/territory organisations, etc.

- ABARES; Bureau of Meteorology; Commonwealth Scientific and Industrial Research Organisation; Department of Agriculture, Fisheries and Forestry; Geoscience Australia; Murray-Darling Basin Authority; state/territory organisations, etc.

Changes made to Figure 23.3 Integrating information systems - Primary institutional responsibilities

From 28/10/2024,

Footnotes

- References to the Department of Industry, Science, Energy and Resources have been changed to Department of Climate Change, Energy, the Environment and Water.

- References to the Department of Agriculture, Water and Environment have been changed to Department of Agriculture, Fisheries and Forestry.

- This reflects current administrative arrangements.

ABS integrated Environmental-Economic Accounts

Introduction

23.231 Over the last twenty years, the ABS has produced a range of individual environmental accounts, including accounts for water, energy, waste, land, fish and environmental taxes. The ABS program of environmental accounts is evolving and intends to produce environmental accounts across a greater range of dimensions on a regular basis. This will support the great analytical power of integrated comparisons across dimensions and over time.

23.232 A range of Australian organisations produce environmental accounts. These include the Bureau of Meteorology (National Water Account); Department of Climate Change, Energy, the Environment and Water (energy balances, GHG emissions accounts); the Wentworth Group (regional accounts); and the Department of Agriculture, Fisheries and Forestry (ecosystem accounts). While the degree varies, each of these accounts has links to the SEEA. These accounts are compiled using either Australian principles, such as the Australian Water Accounting Standards (BoM), or as a part of international efforts to monitor particular pressures, such as the GHG emission accounts (DCCEEW).

23.233 A variety of environmental accounts have been compiled by the ABS. These accounts are at different stages of maturity, and some accounts that have been compiled in the past, such as environment protection expenditure accounts, are no longer produced. Other ones are in regular annual production, such as the natural resources on the national balance sheet, or energy and water accounts.

23.234 In some cases, the ABS undertakes substantial primary data collection activity to support the production of accounts, such as for the Water Accounts Australia. In other cases, the ABS does not undertake the primary data collections. For example, the ABS reconfigures existing data for the Energy Account from the energy balances and and emissions data compiled by DICCEEW to match with SEEA and SNA concepts.

ABS collections

23.235 Below is a very brief listing of current and proposed ABS environmental-economic accounts - their key features, followed by a table outlining expected timeframes for their future release.

- Water Account, Australia – annual publication, includes information on the physical and monetary supply and use of water in the Australian economy. It also includes information on water use and consumptive practices of key industries (Agriculture, Water supply, sewerage and drainage services) and households, as well as presenting data cubes for Australia and the States and Territories.

- Energy Account, Australia – annual publication, includes physical supply and use tables that identify physical volumes by industry and energy product; hybrid supply and use estimates; that is, accounts that present related data in both monetary and physical units; physical energy asset tables that identify economically demonstrated reserves of non-renewable primary energy assets; and energy indicators including energy intensity and energy use per household.

- Land Account: land accounts have been produced on an ad hoc basis for various regions and states, including Queensland, South Australia, Victoria and the Great Barrier Reef Region – these accounts include physical and monetary land use by industry, land cover by industry and changes in land cover over time. In addition, land accounts could potentially include terrestrial biodiversity and carbon. The ABS and DAWE are developing a set of National land accounts for release in 2021.

- Waste Account, Australia –presents integrated monetary and physical waste information using an internationally recognised conceptual framework to assist in informing waste policy and discussion in Australia.

- Experimental Environmental-Economic Accounts for the Great Barrier Reef – one-off publication, includes a wide range of environmental-economic accounts, including: marine and terrestrial extent and condition; biodiversity; expenditure on environmental goods and services; provisioning ecosystem services for agriculture, forestry, fishing and aquaculture; regulating ecosystem services; tourism cultural services; water; and carbon.

- From Nature to the Table: Environmental-Economic Accounting for Agriculture – one-off publication representing the first experimental step by the ABS and its data partners to implement the international SEEA for Australia’s agriculture, forestry and fishing industries.

23.236 Other types of accounts, such as those for emissions and material flows, EPE accounts, as well as the classification and valuation of natural resource assets will be addressed in a research agenda.

23.237 Table 23.1 provides a summary of current ABS environmental-economic accounts.

| Theme | Stock | Flow | Environmentally Related Transaction |

|---|---|---|---|

| Water | ✔ Physical, Monetary and Emissions | ||

| Energy | ✔ Physical and Monetary | ✔ Physical, Monetary and Emissions | |

| Minerals | ✔ Physical and Monetary | ✔ Physical only | |

| Timber | ✔ Monetary | ||

| Fish | ✔ Physical only | ✔ Physical only | |

| Waste | ✔ Physical and Monetary | ||

| Greenhouse gas emissions | ✔ Physical only | ||

| Land cover and land use (sub national) | ✔ Monetary and Spatial | ||

| Environmental Taxes | ✔ Monetary only | ||

| Environmental Protection Expenditure | ✔ Monetary only |

Addressing public policy issues

23.229 There has been a significant amount of work done recently to provide data to inform the various public policy debates concerning the environment in Australia and the SEEA framework has been integral to this process. In April 2018 the Australian Government and all states and territory governments agreed on a National Strategy and Action Plan to implement EEA across Australia. The Strategy and Action Plan builds on the efforts of the ABS, and state and territory governments to deliver a nationally consistent approach to Environmental-Economic Accounting.